Investing for Beginners: A Comprehensive Guide to Growing Your Wealth

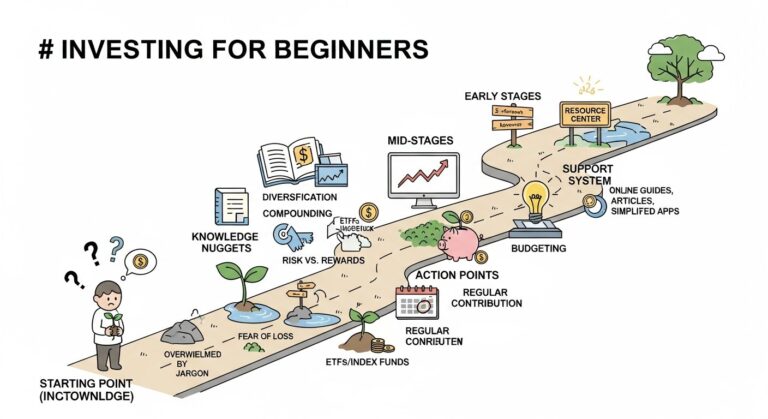

Embarking on the journey of investing for beginners can initially seem daunting, filled with unfamiliar jargon and numerous choices. However, grasping the fundamentals of investing is not only accessible but absolutely essential for building long-term financial security. Investing involves strategically allocating resources, typically money, with the expectation of generating income or profit over time. It’s a powerful financial tool that enables your money to actively work for you, effectively counteracting the erosive effects of inflation and paving a clear path toward achieving significant financial goals, whether it’s buying a home or securing a comfortable retirement.

This comprehensive guide is specifically designed to demystify investing for beginners. We will meticulously break down core investment concepts, explore various accessible investment vehicles, walk you through the practical steps of opening investment accounts, and equip you with proven strategies to confidently build and manage your very first investment portfolio. Our ultimate aim is to transform the often-intimidating prospect of investing into an empowering and manageable process, ensuring you have all the necessary knowledge and practical tools to effectively begin your wealth-building journey.

Why Should Beginners Start Investing?

Starting to invest as a beginner is one of the most impactful financial decisions you can make. The primary reason is to grow your wealth over time, allowing your money to outpace inflation and achieve significant financial milestones. Procrastinating can mean missing out on substantial compounding growth, making your future goals harder to reach. Investing isn’t just for the wealthy; it’s a fundamental strategy for anyone seeking financial independence and security.

What is the Power of Compound Interest?

The Power of Compound Interest is often referred to as the “eighth wonder of the world” for good reason. It’s the interest you earn not only on your initial investment but also on the accumulated interest from previous periods. For a beginner investor, understanding this concept is paramount because it highlights the immense advantage of starting early. Small, consistent investments made over a long time horizon can grow exponentially, leading to substantial wealth accumulation. The longer your money is invested, the more time it has to compound, transforming modest contributions into significant sums.

How Does Investing Help Beat Inflation and Grow Wealth?

Inflation is the rate at which the general level of prices for goods and services is rising, and subsequently, the purchasing power of currency is falling. If your money simply sits in a standard savings account, its value is slowly eroded by inflation. Investing, particularly in assets that historically offer higher returns than inflation, is essential for preserving and growing your purchasing power. By investing, you aim to achieve returns that not only cover the cost of inflation but also provide real growth, increasing your net worth over time.

How Can Investing Help Achieve Your Financial Goals?

Whether your financial goals include purchasing a home, funding your children’s education, starting a business, or retiring comfortably, investing provides the pathway to make these aspirations a reality. Different investment strategies and vehicles can be tailored to match specific goals and their associated time horizons. For instance, long-term goals like retirement benefit from growth-oriented investments, while shorter-term goals might require more conservative approaches. Defining your goals early helps guide your investment decisions and motivates consistent saving.

What Core Investment Concepts Should Beginners Understand?

Before diving into specific investment vehicles, it’s crucial for beginners to grasp several fundamental concepts that underpin all successful investing. These ideas will shape your strategy and help you make informed decisions aligned with your financial personality and objectives.

What is Risk Tolerance and Why Does It Matter?

Risk tolerance refers to an individual’s willingness and ability to take on financial risk. It’s a critical attribute for any beginner investor to understand, as it directly influences the types of investments you should consider. Someone with a high-risk tolerance might be comfortable with more volatile assets like growth stocks, accepting potential short-term losses for higher long-term gains. Conversely, a low-risk tolerance might lead an investor towards more stable assets like bonds or high-yield savings accounts. Factors influencing risk tolerance include your financial goals, time horizon, income stability, and personal comfort level with uncertainty. Accurately assessing your risk tolerance helps prevent panic selling during market downturns and ensures your portfolio aligns with your comfort zone.

What is Diversification and How Does It Spread Your Investments?

Diversification is an investment strategy that mitigates risk by investing in a variety of assets. The core principle is “don’t put all your eggs in one basket.” By spreading your investments across different asset classes (like stocks, bonds, real estate), industries, and geographical regions, you reduce the impact of any single investment performing poorly. If one part of your portfolio declines, other parts may be performing well, thus smoothing out overall returns. Effective diversification is a cornerstone of responsible portfolio management for any beginner investor.

What are Time Horizon and Liquidity in Investing?

Your time horizon is the length of time you plan to hold an investment before you need the money. This attribute significantly impacts your investment choices. A longer time horizon (e.g., 20+ years for retirement) allows you to take on more risk, as you have more time to recover from market fluctuations. A shorter time horizon (e.g., 3-5 years for a down payment) typically calls for lower-risk, more liquid investments. Liquidity refers to how easily an investment can be converted into cash without affecting its market price. Highly liquid assets, like savings accounts or money market funds, are good for short-term needs, while less liquid assets, like real estate, are better suited for long-term goals.

How Do Volatility and Market Cycles Impact Investing?

Volatility refers to the rate at which the price of a security or market index changes over a given period. High volatility means prices fluctuate widely, while low volatility means prices are more stable. While volatility can be intimidating for beginners, it’s a natural part of investing. Markets operate in cycles, experiencing periods of growth (bull markets) and decline (bear markets). Understanding that these cycles are normal and temporary can help investors maintain a long-term perspective and avoid making impulsive decisions based on short-term market movements. A long-term perspective, combined with a diversified portfolio, helps weather volatile periods.

What Are Key Investment Vehicles for Beginners?

With an understanding of core concepts, let’s explore the primary investment vehicles accessible to beginners. Each offers distinct characteristics in terms of risk, potential return, and suitability for different financial goals.

What are Stocks and How Do You Own a Piece of a Company?

When you buy a stock, you purchase a small ownership share, or “equity,” in a publicly traded company. As a shareholder, you can benefit in two main ways: through capital appreciation (the stock’s price increases) and through dividends (a portion of the company’s profits paid out to shareholders). Stocks offer the potential for significant long-term growth but also come with higher volatility compared to bonds. Factors like company performance, industry trends, and overall market sentiment influence stock prices. Growth stocks focus on companies expected to grow faster than the market, while value stocks focus on undervalued companies. Market capitalization refers to the total value of a company’s outstanding shares, indicating its size.

What are Bonds and How Do They Provide Income?

Bonds are essentially loans you make to governments (government bonds) or corporations (corporate bonds). In return, the issuer promises to pay you regular interest payments (fixed income) over a specified period, and then repay your principal amount at the maturity date. Bonds are generally considered less risky than stocks and provide a more predictable income stream, making them suitable for beginners looking for stability or income. Their value can be affected by changes in interest rates and the issuer’s credit rating, which indicates their ability to repay the debt.

How Do Mutual Funds & ETFs Offer Instant Diversification?

For beginners, mutual funds and Exchange-Traded Funds (ETFs) are excellent ways to achieve instant diversification without having to buy individual stocks or bonds. Both are professionally managed collections, or “baskets,” of various securities.

- Mutual Funds: These funds pool money from many investors to buy a diversified portfolio of stocks, bonds, or other assets. They are typically bought and sold at the end of each trading day at their Net Asset Value (NAV). Actively managed funds involve fund managers making decisions, while passively managed index funds aim to track a specific market index (like the S&P 500).

- ETFs: Similar to mutual funds, but they trade on stock exchanges throughout the day, just like individual stocks. Most ETFs are passively managed index funds, offering broad market exposure, low expense ratios (annual fees), and transparency. Sector ETFs focus on specific industries.

Both mutual funds and ETFs are highly recommended for new investors due to their built-in diversification and professional management, simplifying the investment process significantly.

What are Robo-Advisors and How Do They Simplify Investing?

Robo-advisors are digital platforms that provide automated, algorithm-driven financial planning services with little to no human supervision. They are particularly appealing to beginner investors because they offer low-cost portfolio management, often with very low minimum investment requirements. After you answer a series of questions about your financial goals and risk tolerance, the robo-advisor will construct and manage a diversified portfolio for you, automatically rebalancing it over time. They are an accessible entry point for those intimidated by traditional investing or who prefer a hands-off approach, though it’s important to understand robo-advisor fees.

| Investment Type | Typical Risk Level | Potential Return | Liquidity | Minimum Investment | Best For |

|---|---|---|---|---|---|

| Stocks | High | High long-term growth | High (most publicly traded) | Low (can buy fractional shares) | Long-term growth, active participation |

| Bonds | Low to Medium | Moderate, steady income | Medium | Medium (can vary) | Capital preservation, income, diversification |

| Mutual Funds | Medium to High | Medium to High long-term growth | Low (traded once daily) | Medium (often $1000+) | Diversification, professional management |

| ETFs | Medium to High | Medium to High long-term growth | High (traded throughout day) | Low (can buy fractional shares) | Diversification, low fees, flexibility |

| High-Yield Savings Accounts | Very Low | Low, stable interest | Very High | Very Low (often $0) | Emergency funds, short-term savings (contextual) |

How Do I Open an Investment Account?

Opening an investment account is the practical first step to putting your money to work. This process has become significantly easier and more accessible for beginners, with numerous options available. Understanding the different types of accounts and choosing the right one for your needs is crucial.

How to Choose the Right Brokerage Account?

A brokerage account is simply an account you open with a brokerage firm that allows you to buy and sell investments like stocks, bonds, mutual funds, and ETFs. For beginners, choosing the right brokerage account often comes down to ease of use, fees, available investment options, and customer support. Many reputable online brokerages offer user-friendly platforms, educational resources, and commission-free trades for stocks and ETFs. When choosing, consider factors like minimum deposit requirements, research tools, and whether they offer fractional shares, which allow you to invest small amounts into expensive stocks.

What are Retirement Accounts like 401(k)s and IRAs?

Retirement accounts are specifically designed to help you save for retirement with significant tax advantages. These are often the first investment accounts beginners encounter.

- 401(k)s: Employer-sponsored retirement plans. Contributions are often pre-tax, reducing your current taxable income. Many employers offer a 401(k) matching contribution, which is essentially free money and a powerful incentive to participate. You choose from a selection of funds offered by your plan administrator.

- Individual Retirement Arrangements (IRAs): You can open an IRA independently of an employer.

- Traditional IRA: Contributions may be tax-deductible in the contribution year, and earnings grow tax-deferred until withdrawal in retirement.

- Roth IRA: Contributions are made with after-tax money, but qualified withdrawals in retirement are tax-free. This is often an excellent option for beginners who anticipate being in a higher tax bracket in retirement.

Understanding IRA contribution limits and withdrawal rules is important.

What is the Difference Between Taxable vs. Tax-Advantaged Accounts?

The distinction between taxable brokerage accounts and tax-advantaged retirement accounts is vital for beginner investors.

- Taxable Brokerage Account: You pay taxes on any capital gains (profits from selling an investment) and dividends in the year they are realized. These offer maximum flexibility, as you can withdraw funds at any time without penalty, making them suitable for non-retirement goals.

- Tax-Advantaged Accounts (e.g., 401(k)s, IRAs): These accounts offer specific tax benefits, such as tax-deductible contributions (Traditional IRA/401k) or tax-free withdrawals in retirement (Roth IRA). However, they come with restrictions, such as contribution limits and penalties for early withdrawals (before retirement age). For beginners, maximizing contributions to tax-advantaged accounts, especially with employer matches, should generally be a priority due to the significant long-term tax benefits.

| Account Type | Purpose | Tax Treatment | Contribution Limits (as of 2026/omitted) | Withdrawal Rules | Best For |

|---|---|---|---|---|---|

| Taxable Brokerage Account | Any financial goal (short- or long-term) | Capital gains & dividends taxed annually | No IRS limits (broker minimums may apply) | Flexible, no age restrictions or penalties | Savings beyond retirement, accessible funds |

| Traditional IRA | Retirement savings | Pre-tax contributions possible; tax-deferred growth; taxed upon withdrawal | Annual limit (e.g., $7,000 for under 50) | Penalties for early withdrawal (before 59½) | Reducing current taxable income, expecting lower tax bracket in retirement |

| Roth IRA | Retirement savings | After-tax contributions; tax-free growth; tax-free qualified withdrawals | Annual limit (e.g., $7,000 for under 50, income limits apply) | Contributions can be withdrawn tax/penalty-free anytime; earnings have rules | Expecting higher tax bracket in retirement, tax-free income later |

How Can Beginners Build Their First Investment Portfolio?

Once you have your investment accounts set up, the next step for a beginner investor is to construct a portfolio that aligns with your financial goals, risk tolerance, and time horizon. This involves making strategic decisions about how to allocate your assets and how to manage them over time.

What is Asset Allocation and How Does It Determine Your Investment Mix?

Asset allocation is the process of deciding how to divide your investment portfolio among different asset categories, such as stocks, bonds, and cash equivalents. This is one of the most important decisions you’ll make, as it largely determines your portfolio’s risk and return characteristics. For a beginner with a long time horizon, a higher allocation to stocks (e.g., 70-80%) might be appropriate due to their higher growth potential. As you approach a goal or retirement, you might shift towards a more conservative mix with a higher allocation to bonds for stability. Your asset allocation should be regularly reviewed and adjusted as your circumstances change.

How Does Dollar-Cost Averaging Help Beginners Invest Consistently?

Dollar-cost averaging (DCA) is a simple yet powerful strategy for beginner investors. It involves investing a fixed amount of money at regular intervals (e.g., $100 every month), regardless of market fluctuations. This approach has several benefits:

- It reduces the impact of volatility: When prices are high, your fixed amount buys fewer shares; when prices are low, it buys more shares. Over time, your average cost per share tends to be lower.

- It removes emotional decision-making: You stick to a plan rather than trying to time the market, which is notoriously difficult even for experts.

- It encourages consistent saving: By automating your investments, you build a disciplined habit.

DCA is an excellent strategy for beginners, especially when investing in volatile assets like stocks or stock-based funds.

Why is Portfolio Rebalancing Important for Staying on Track?

Over time, the market performance of your different assets can cause your portfolio’s original asset allocation to drift. For example, if your stocks perform exceptionally well, they might grow to represent a larger percentage of your portfolio than you initially intended, increasing your overall risk. Portfolio rebalancing is the process of adjusting your portfolio back to your target asset allocation. This typically involves selling some of your overperforming assets and using the proceeds to buy more of your underperforming assets. Rebalancing frequency can be annual or semi-annual, or triggered when an asset class deviates significantly from its target weight. It helps maintain your desired risk level and ensures you’re not unknowingly taking on too much or too little risk.

What are the Risks of Investing and How Can I Manage Them?

Investing inherently involves risk, but for beginners, understanding these risks and how to manage them is key to successful long-term growth. Ignoring potential downsides can lead to costly mistakes and discourage future investment.

What Common Investing Mistakes Should Beginners Avoid?

Beginners often fall prey to several common pitfalls. Avoiding these can significantly improve your chances of success:

- Timing the Market: Trying to predict market tops and bottoms is nearly impossible and often leads to missing out on significant gains.

- Emotional Investing: Panic selling during downturns or buying into “hot” trends without research can be detrimental. Stick to your plan.

- Lack of Diversification: Concentrating all your investments in one stock or sector exposes you to unnecessary risk.

- Ignoring Fees: High expense ratios on funds or excessive trading fees can eat into your returns over time.

- Not Having an Emergency Fund: Investing money you might need soon means you could be forced to sell assets at a loss.

- Failing to Rebalance: Allowing your portfolio to drift from your target allocation can expose you to unintended risk.

- Impatience: Investing is a long-term game. Expecting quick riches often leads to speculative, high-risk behavior.

Why are Long-Term Perspective and Emotional Discipline Important for Investors?

One of the most powerful tools a beginner investor can wield is a long-term perspective. Financial markets are dynamic, experiencing both bull markets (periods of sustained growth) and bear markets (periods of decline). Short-term fluctuations, or volatility, are normal. Those who succeed in investing understand that these ups and downs are part of the journey and maintain emotional discipline, resisting the urge to react impulsively to market news or downturns. Focus on your long-term goals, trust your diversified strategy, and remember that time in the market often beats timing the market.

When Should You Consider Consulting a Financial Professional?

While this guide provides a solid foundation, some beginners may benefit from professional guidance. A qualified financial advisor, such as a Certified Financial Planner (CFP), can help you assess your risk tolerance, define your goals, create a personalized investment plan, and navigate complex financial situations. They can also provide insights into specific products and strategies tailored to your unique circumstances. When seeking advice, ensure the advisor is a fiduciary, meaning they are legally obligated to act in your best interest. Resources from entities like the SEC (Securities and Exchange Commission) and FINRA (Financial Industry Regulatory Authority) can help you verify credentials and find reputable professionals.

How Much Money Do I Need to Start Investing?

A common misconception among beginners is that you need a large sum of money to start investing. This is simply not true. Thanks to modern investment platforms and options, investing is more accessible than ever, even with small amounts.

Can You Start Investing with Small Amounts and Grow Over Time?

You can start investing with surprisingly little money. Many online brokerage accounts and robo-advisors have no minimum deposit requirements or allow you to start with as little as $5 to $100. Fractional shares, offered by many platforms, allow you to buy a portion of a high-priced stock or ETF for a fraction of the cost. The key is not the initial amount, but rather the consistency and discipline of regular contributions, combined with the power of compound interest. Even $25 or $50 consistently invested each month can grow significantly over decades.

Why Prioritize Debt Elimination and Emergency Savings Before Investing?

Before you commit to investing, it’s crucial for beginners to establish a strong financial foundation. This involves two critical steps:

- Eliminate High-Interest Debt: Debts like credit card balances or high-interest personal loans often carry interest rates far higher than typical investment returns. Paying these off should be a top priority, as it guarantees a return on your money equal to the interest rate you avoid.

- Build an Emergency Fund: Maintain an easily accessible fund (e.g., in a high-yield savings account) covering 3-6 months of essential living expenses. This fund acts as a financial safety net, preventing you from having to sell investments at an inopportune time during an unexpected expense or job loss. Investing should only begin after these foundational steps are in place.

What Are the Next Steps for Your Investment Journey?

Congratulations! By reaching this point, you’ve gained a foundational understanding of investing for beginners. But the journey doesn’t end here; it evolves. Continuous learning and adaptation are key to long-term success in the financial markets.

Why is Continuous Learning and Adaptation Important in Investing?

The financial world is constantly changing, with new products, regulations, and economic shifts. For a beginner investor, commitment to continuous learning is vital. Stay informed about market trends, economic indicators, and personal finance best practices. Read reputable financial news, books, and educational articles. Revisit your investment plan periodically, perhaps annually, to ensure it still aligns with your evolving goals, risk tolerance, and life circumstances. Remember, the best investors are always learning.

How Can You Leverage Expert Resources and Tools for Investing?

The internet offers a wealth of resources to support your investment journey.

- Financial News Websites: Follow sites like The Wall Street Journal, Bloomberg, or even reputable personal finance blogs.

- Brokerage Research: Most online brokerages provide extensive research reports, educational articles, and tools for their customers.

- Government Resources: Official websites of the SEC (Securities and Exchange Commission) and FINRA (Financial Industry Regulatory Authority) offer investor alerts and educational materials. The IRS website is essential for tax-related information.

- Financial Calculators: Utilize online calculators for compound interest, retirement planning, or investment goal tracking.

- Books and Podcasts: Explore classic investment books and reputable financial podcasts for deeper insights and diverse perspectives.

Don’t be afraid to leverage these tools to enhance your knowledge and refine your strategies.

| Term | Definition | Importance for Beginners |

|---|---|---|

| Inflation | The rate at which prices for goods and services increase, leading to a fall in purchasing power. | Explains why investing is crucial to grow money beyond just saving. |

| Compound Interest | Interest earned on both the initial principal and the accumulated interest from previous periods. | Highlights the power of starting early and consistent investing for exponential growth. |

| Diversification | Spreading investments across various assets to minimize risk. | A fundamental strategy to protect your portfolio from significant losses in one area. |

| Volatility | The degree of variation of a trading price series over time (how much prices fluctuate). | Helps beginners understand market ups and downs are normal and to maintain a long-term view. |

| Asset Allocation | The strategy of dividing an investment portfolio among different asset categories (e.g., stocks, bonds, cash). | Key to defining your portfolio’s risk/return profile and matching it to your goals. |

| Expense Ratio | The annual fee charged by mutual funds and ETFs for management and other operating costs, expressed as a percentage of assets. | Crucial to consider as even small percentages can significantly impact long-term returns. |

| Bull Market | A period in financial markets when prices are rising or are expected to rise. | Indicates periods of investor optimism and economic growth; helps contextualize market cycles. |

| Bear Market | A market in which prices are falling, encouraging selling. | Indicates periods of investor pessimism; an opportunity to buy assets at lower prices for long-term investors. |

Investing for beginners is a journey of continuous learning and strategic action. By understanding the core concepts, choosing appropriate investment vehicles, setting up the right accounts, and employing sound portfolio management techniques, you are well on your way to building a secure financial future. Remember to start early, stay diversified, invest consistently, and maintain a long-term perspective. The financial world awaits your disciplined and informed participation.

Last Updated: March 28, 2026

Author Bio: Jane Doe is a Certified Financial Planner (CFP) and holds an MBA in Finance, with over a decade of experience guiding individuals and families toward their financial goals. She specializes in accessible investment strategies for new investors and has contributed to numerous financial literacy initiatives, making complex financial topics understandable for beginners.