Your Ultimate Personal Finance Guide for Beginners: Master Your Money Effectively

Embarking on your financial journey can feel daunting, but with the right guidance, mastering your money becomes an empowering reality. This **ultimate personal finance guide for beginners** is meticulously crafted to equip you with the foundational knowledge and actionable strategies needed to take control of your finances. For individuals new to money management, understanding personal finance isn’t just about balancing a checkbook; it’s about building a secure future, achieving your aspirations, and even enhancing your career development. We’ll cover everything from creating a budget and building savings to intelligently managing debt and making your first investments, all while emphasizing the crucial link between sound financial practices and a thriving professional life. Prepare to transform your relationship with money and lay a robust foundation for lasting financial security.

What is Personal Finance and Why is it Crucial for Beginners?

To truly master your money, a **beginner** must first understand: What is Personal Finance and Why is it Crucial for Beginners? At its core, **personal finance** encompasses all financial decisions and activities of an individual or household, including budgeting, saving, investing, and spending. For **beginners**, grasping these principles is not just about managing money, but about laying a robust foundation for future financial security and enabling opportunities for career development. It involves planning for your present needs while strategically preparing for your future financial goals, ensuring you retain control over your economic destiny. Financial literacy, especially for beginners, is a cornerstone of long-term well-being.

Defining Personal Finance: More Than Just Money

**Personal finance** is the application of financial principles to an individual’s monetary decisions. It’s about how **individuals** manage their resources, including their income, expenses, investments, and debts. The goal is to optimize one’s financial situation to achieve specific life goals, such as buying a home, retiring comfortably, or funding education. It’s a proactive approach to wealth management that directly impacts an individual’s quality of life and future opportunities. Understanding these fundamental principles empowers you to make informed choices rather than simply reacting to financial circumstances. This proactive management is key to sustained financial health.

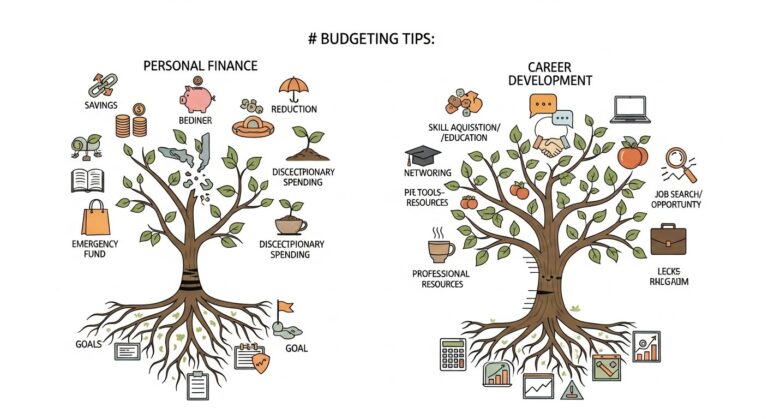

The Core Pillars of Financial Well-being for Beginners

For any **beginner**, building financial well-being rests upon several key pillars:

- Budgeting and Cash Flow Management: This involves tracking your income and expenses to understand where your money goes. A well-structured budget empowers you to allocate funds effectively.

- Saving and Emergency Funds: Prioritizing savings for unexpected events and future goals is paramount. An emergency fund provides a crucial financial safety net.

- Debt Management: Learning to manage and reduce debt efficiently, distinguishing between ‘good’ and ‘bad’ debt, is vital for long-term financial health.

- Investing for Growth: Making your money work for you through smart investments helps build wealth over time. This offers the potential for significant long-term growth.

- Financial Planning and Goal Setting: Defining clear financial goals, such as buying a home or retirement, guides your financial decisions and creates a roadmap for success.

Why Do Beginners Need a Personal Finance Guide?

For **individuals** just starting their independent financial journey, a comprehensive guide is indispensable. Without a clear understanding of financial concepts, **beginners** often make common mistakes that can hinder their progress for years. This guide provides a structured pathway to financial literacy, helping you avoid pitfalls and build positive money habits from the outset. It ensures that your early financial decisions are strategic, leading to greater financial security and opening doors for significant career development opportunities down the line. A proactive approach to learning about personal finance today sets the stage for a prosperous tomorrow. As financial experts often state, early financial education is a strong predictor of future wealth accumulation. Source: Financial Literacy Study 2023

What are the Key Steps to Building Your Financial Foundation?

Building on the foundational understanding of what **personal finance** entails, the next crucial step for **beginners** is to establish a solid financial foundation. This involves practical, actionable steps that create the framework for all future financial success. By mastering these key steps, **you** gain immediate control over your money, setting the stage for achieving your financial goals and empowering your overall financial journey.

Understanding Your Income and Expenses for Beginners

The first step in any sound financial plan is to gain clarity on your cash flow. **Individuals** must accurately identify all sources of **income** and meticulously track all **expenses**. This process reveals exactly how much money enters your accounts and precisely where it is spent. Distinguishing between **fixed costs** (like rent or loan payments) and **variable costs** (such as groceries or entertainment) is critical. This initial assessment provides the raw data needed to construct an effective budget and empowers you to make informed decisions about your spending habits. Many financial advisors recommend a detailed expense tracking period of at least one month to get an accurate picture.

How Do I Create a Realistic Budget as a Beginner?

Creating a **realistic budget** is the cornerstone of effective money management for **beginners**. A budget helps you allocate your income, prioritize spending, and work towards your financial goals. It empowers you to gain control over your money rather than letting your money control you. Here are 5 steps to create your first budget:

- Calculate Your Monthly Net Income: Tally all income sources after taxes and deductions. This is the total amount you have available to spend and save.

- Track Your Expenses: For one month, meticulously record every single expense. Categorize them into essentials (housing, food, transport) and non-essentials (entertainment, dining out). Using **tracking apps** or a simple spreadsheet can greatly simplify this process.

- Categorize and Analyze Your Spending: Review your tracked expenses. Identify areas where you might be overspending and opportunities for reduction. This analysis empowers you to make intentional spending choices.

- Set Spending Limits: Based on your income and expense analysis, allocate specific amounts to each spending category. Be realistic to ensure sustainability. Common budgeting methods like the **50/30/20 rule** (50% needs, 30% wants, 20% savings/debt) or **zero-based budgeting** can guide this step.

- Monitor and Adjust: A budget isn’t static; it’s a living document. Regularly review your budget to ensure it aligns with your income, expenses, and financial goals. Adjustments are natural and necessary as your financial situation evolves.

Table 1: Budgeting Methods Comparison for Beginners

| Budgeting Method | Description | Pros | Cons | Best For |

|---|---|---|---|---|

| 50/30/20 Rule | Allocates 50% of income to needs, 30% to wants, and 20% to savings & debt repayment. |

|

|

Beginners seeking a straightforward, balanced approach. |

| Zero-Based Budgeting | Assigns every dollar of income a specific job (spending, saving, debt repayment) until your income minus your expenses equals zero. |

|

|

Individuals who want full control over every dollar and clarity on spending. |

| Envelope System | Uses physical cash in envelopes for specific spending categories, restricting spending to the allocated cash. |

|

|

Those who struggle with overspending on variable expenses and prefer a tangible method. |

The Power of Saving: How to Build an Emergency Fund as a Beginner

Once you have a budget in place, prioritizing **saving** becomes the next critical step for **beginners**. The concept of an emergency fund is paramount: it is a dedicated savings account specifically for unexpected expenses, such as job loss, medical emergencies, or urgent home repairs. This fund acts as a vital financial safety net, reducing stress and preventing you from incurring high-interest debt when unforeseen events occur. Financial experts recommend saving at least three to six months’ worth of essential living expenses in an easily accessible **high-yield savings account**. Setting up **automation** for savings, where a portion of your paycheck is automatically transferred to your savings account, is an effective strategy to consistently build this fund without conscious effort. This proactive approach to saving empowers you to navigate life’s uncertainties with confidence.

Benefits of an Emergency Fund:

- Reduces Financial Stress: Knowing you have a buffer provides peace of mind.

- Prevents Debt: Avoids resorting to credit cards or loans for emergencies.

- Increases Financial Security: Creates a stable foundation for future financial growth.

- Offers Flexibility: Provides options during unforeseen career transitions or personal events.

How Can Beginners Master Debt: From Burden to Leverage?

With a solid budget and growing savings, **beginners** are ready to tackle one of the most significant obstacles to financial freedom: debt. Understanding and effectively managing **debt** is not just about paying it off; it’s about transforming it from a potential burden into a manageable tool, or even a leverage point for future growth. This section empowers **individuals** to approach debt strategically, reducing its impact and paving the way for greater financial security.

Good Debt vs. Bad Debt: A Beginner’s Perspective

Not all debt is created equal. For **beginners**, distinguishing between ‘good debt’ and ‘bad debt’ is a crucial concept. **Good debt** is typically an investment that has the potential to increase your net worth or generate future income. Examples include a **mortgage** on a home (which can appreciate in value), **student loans** for education (which can lead to higher earning potential and career development), or a small business loan. These debts often come with lower interest rates and provide a tangible return. Conversely, **bad debt** is debt incurred for depreciating assets or consumption, especially with high interest rates. This includes most **credit card** debt, personal loans for consumer goods, or car loans for rapidly depreciating vehicles. These types of debt drain your finances without providing long-term value, making them a significant obstacle to financial progress. Understanding this distinction is a fundamental step in personal finance.

Understanding Your Credit Score and Report as a Beginner

Your credit score and **credit report** are vital components of your financial identity, especially for **beginners**. A **credit score** is a three-digit number that represents your creditworthiness, influencing your ability to secure loans, rent an apartment, or even get certain jobs. A good **credit score** (typically above 670) offers access to better interest rates and more favorable loan terms. Your **credit report**, on the other hand, is a detailed history of your borrowing and repayment activities, compiled by credit bureaus. It includes information on your loans, credit cards, payment history, and any delinquencies. Regularly reviewing your **credit report** ensures accuracy and helps identify potential fraud. Building a positive credit history through timely payments and responsible credit use is essential for long-term financial health and unlocks significant financial opportunities. Source: Consumer Financial Protection Bureau

What are Effective Strategies to Pay Off Debt for Beginners?

For **beginners** overwhelmed by debt, implementing a clear repayment strategy is key. These strategies empower **individuals** to systematically reduce their debt burden and save on interest. The goal is to make debt repayment a structured and achievable process.

- List All Debts: Compile a comprehensive list of all your debts, including the creditor, outstanding balance, interest rate, and minimum monthly payment. This provides a clear overview of your financial obligations.

- Choose a Repayment Strategy: Two popular methods are the **debt snowball** and **debt avalanche**. The debt snowball focuses on paying off the smallest balance first for motivational wins, while the debt avalanche targets the highest interest rate debt first to save the most money on interest.

- Make More Than the Minimum Payments: Wherever possible, paying more than the minimum due significantly reduces the total interest paid and accelerates your debt-free date.

- Consider Debt Consolidation or Refinancing: For high-interest debts, consolidating multiple debts into one loan with a lower interest rate, or refinancing an existing loan, can simplify payments and reduce overall cost. Evaluate the terms carefully.

- Avoid New Debt: While actively paying down existing debt, commit to not incurring new, unnecessary debt. This prevents the cycle from perpetuating and allows you to gain true financial traction.

Table 2: Debt Repayment Strategies for Beginners

| Strategy | Description | Focus | Potential Benefit | Best For |

|---|---|---|---|---|

| Debt Snowball | Pay minimums on all debts except the smallest one, which you attack with extra payments. Once paid off, roll that payment amount into the next smallest debt. | Psychological wins and motivation. | Builds momentum and keeps you motivated through quick wins. | Beginners who need motivation and encouragement to stay on track. |

| Debt Avalanche | Pay minimums on all debts except the one with the highest interest rate, which you attack with extra payments. Once paid off, roll that payment amount into the debt with the next highest interest rate. | Financial efficiency (saving interest). | Minimizes the total amount of interest paid over the long term. | Individuals who are disciplined and prioritize saving money on interest. |

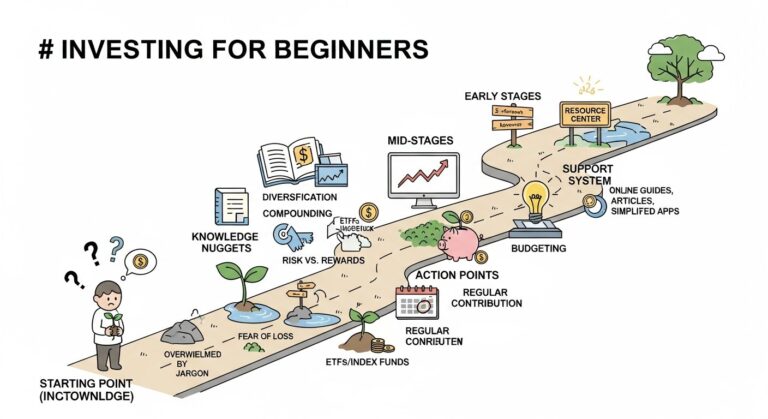

How Can Beginners Start Investing Wisely?

Once **beginners** have established a budget, built an emergency fund, and begun to manage debt, the natural next step in the **personal finance** journey is to explore investing. **Investing** allows your money to grow over time, potentially outpacing inflation and significantly contributing to your long-term financial goals. For **individuals** just starting, the world of investments can seem complex, but by focusing on fundamental concepts and understanding manageable options, you can begin to build wealth wisely.

The Basics of Investing: Growth and Risk for Beginners

At its core, **investing** means committing money or capital to an endeavor with the expectation of obtaining an additional income or profit. The primary goal for **beginners** is typically **long-term growth** of wealth. However, investing always involves an element of **risk**. The potential for higher returns often comes with higher risk, while lower-risk investments typically offer more modest returns. Key concepts include:

- Compound Interest: The magic of earning returns on your initial investment plus the accumulated interest from previous periods. This is a powerful force for wealth creation over time.

- Diversification: Spreading your investments across various asset classes to reduce risk. This strategy ensures that a downturn in one area doesn’t decimate your entire portfolio.

- Risk Tolerance: Understanding your comfort level with potential losses. This personal assessment guides your investment choices.

What are Common Types of Investments for Beginners?

For **beginners**, starting with accessible and relatively straightforward investment vehicles is advisable. These options provide a good entry point into the market while managing risk:

- High-Yield Savings Accounts (HYSAs): While not strictly an investment, HYSAs offer better interest rates than traditional savings accounts, making them excellent for emergency funds and short-term savings goals. They are low-risk and highly liquid.

- Index Funds and Exchange-Traded Funds (ETFs): These are funds that hold a diversified basket of stocks or bonds, tracking a specific market index (like the S&P 500). They offer instant diversification, low fees, and are generally considered a solid long-term investment for beginners.

- Target-Date Funds: Designed with a specific retirement year in mind, these funds automatically adjust their asset allocation over time, becoming more conservative as you approach your target date. They provide a “set it and forget it” approach, ideal for **beginners** planning for retirement.

- 401(k)s and IRAs: These are tax-advantaged retirement accounts that allow your investments to grow tax-deferred or tax-free. They are powerful tools for long-term wealth building, often with employer matching contributions in the case of a 401(k).

Table 3: Beginner Investment Options

| Investment Type | Risk Level | Potential Return | Liquidity | Best For Beginners |

|---|---|---|---|---|

| High-Yield Savings Account (HYSA) | Low | Modest, typically just above inflation | Very High (easy access to funds) | Emergency funds, short-term goals, or very risk-averse individuals. |

| Index Funds (ETFs) | Medium | Moderate to high, aligns with market growth over long term | High (can be bought/sold daily) | Long-term wealth building, instant diversification, low fees. |

| Target-Date Funds | Medium (adjusts over time) | Moderate to high, designed for retirement growth | Medium (can be sold, but designed for long-term) | Retirement savings, hands-off approach, automatic asset allocation. |

Diversification and Long-Term Vision for Beginner Investors

For **beginners**, the core tenets of investing should be **diversification** and maintaining a **long-term vision**. **Diversification** is paramount; it means not putting all your eggs in one basket. By investing in a variety of assets—different types of stocks, bonds, or even real estate—you reduce the overall risk of your portfolio. If one investment performs poorly, others may perform well, balancing out your returns. Furthermore, understanding the power of **long-term growth** is critical. Market fluctuations are normal, but historically, markets tend to grow over extended periods. **Beginners** should resist the urge to react to short-term market dips and instead focus on consistent contributions and allowing **compound interest** to work its magic over decades. This patient, diversified approach is how true wealth is built. It’s also wise to consider basic tax implications of investing as you progress.

How Can Beginners Set and Achieve Financial Goals?

After establishing foundational financial habits, **beginners** must transition from merely managing money to strategically directing it towards specific aspirations. Setting clear, achievable **financial goals** is the roadmap that guides your entire **personal finance** journey. Without goals, your efforts can lack direction. This section empowers **individuals** to define their financial future and develop a concrete plan for success.

Defining SMART Financial Goals for Beginners

For **beginners**, defining **financial goals** is not enough; these goals must be SMART:

- Specific: Clearly define what you want to achieve. Instead of “save money,” aim for “save for a down payment on a home.”

- Measurable: Quantify your goals. “Save $20,000 for a down payment.” This allows you to track progress.

- Achievable: Set realistic goals based on your income and current financial situation. Stretch goals are good, but impossible goals lead to frustration.

- Relevant: Ensure your goals align with your overall life values and aspirations, including your career development plans.

- Time-bound: Set a deadline for achieving your goal. “Save $20,000 in three years.” This creates urgency and helps with planning.

Examples of SMART goals for **beginners** might include “Build an emergency fund of $5,000 within 12 months” or “Pay off my $3,000 credit card debt within 18 months.” These specific goals provide clear targets for your budgeting and saving efforts. Consider also setting goals related to basic insurance needs like health or life insurance.

Tracking Progress and Adjusting Your Financial Plan as a Beginner

Once **financial goals** are set, consistent **tracking progress** is vital. Regularly review your budget, savings, and investment performance against your established targets. This allows you to see what’s working and what needs adjustment. If you’re falling behind, don’t be discouraged; instead, evaluate your spending, look for new ways to increase income, or consider adjusting the timeline for your goal. Life changes, and so should your financial plan. Flexibility and a willingness to adapt your strategies are hallmarks of effective money management for **individuals** committed to long-term financial success. This iterative process ensures your plan remains relevant and achievable.

How Does Personal Finance Intersect with Career Development?

Having navigated the essential pillars of personal finance, **beginners** are now ready to explore a crucial, often overlooked, dimension: the powerful synergy between sound **personal finance** and successful **career development**. Your financial health directly impacts your professional opportunities, and conversely, strategic career moves can significantly accelerate your financial goals. This section explores how these two central entities, personal finance and career development, are intertwined, offering **individuals** a holistic approach to success.

Investing in Your Skills for Higher Earning Potential

One of the most impactful investments a **beginner** can make is in their own **skill development**. Acquiring new, in-demand skills, pursuing higher education, or obtaining professional certifications can directly lead to **higher earning potential**. This might involve investing in online courses, vocational training, or even a degree. While these investments have upfront costs, the return on investment through increased salary, promotions, and new career opportunities can be substantial. For **individuals** focused on both their personal finance and career development, continuously enhancing your professional value is a strategic move that pays dividends, often allowing you to accelerate savings, reduce debt, and invest more aggressively.

Financial Independence for Career Choice

Achieving a degree of **financial independence** offers profound benefits for your **career choices**. When you have a robust emergency fund, minimal debt, and growing investments, **you** gain the freedom to pursue career paths that align more closely with your passions and values, rather than being solely driven by salary. This could mean taking a lower-paying but more fulfilling job, starting your own business (entrepreneurship), or even taking a sabbatical for further education or personal growth. Financial security empowers **individuals** to negotiate better terms, switch industries, or even take calculated risks that can lead to greater long-term career satisfaction and success, showcasing the true power of integrated financial and career planning.

Entrepreneurship and Passive Income Streams for Beginners

For **beginners** looking to supercharge their **personal finance** and career development, exploring **entrepreneurship** and developing **passive income** streams can be transformative. Entrepreneurship involves starting your own business, leveraging your skills to create value and potentially generate significant income. This often requires careful financial planning and a calculated risk tolerance. Simultaneously, cultivating **passive income** streams—money earned with minimal ongoing effort after the initial setup—can provide financial cushions and accelerate wealth building. Examples include income from rental properties, royalties, dividends from investments, or a successful online course. These strategies not only diversify your income sources but also offer greater flexibility and the potential for true financial independence, allowing for unparalleled control over your career and lifestyle.

What are the Essential Personal Finance Mistakes Beginners Should Avoid?

While this guide emphasizes proactive steps for **beginners** in **personal finance**, it’s equally important to be aware of common pitfalls. Avoiding these mistakes can save **individuals** significant time, stress, and money, ensuring their financial journey remains on track. Understanding these missteps empowers you to navigate the complexities of money management more effectively and secure your financial future.

Why is Ignoring Your Budget a Mistake for Beginners?

One of the most frequent mistakes **beginners** make is creating a **budget** but then failing to stick to it or review it regularly. An unmonitored budget is merely a document, not a tool. Ignoring your budget means losing sight of where your money is going, leading to overspending, unexpected shortfalls, and an inability to meet your financial goals. Consistently tracking income and expenses, and making necessary adjustments, is crucial for the budget to serve its purpose of empowering you to gain control over your finances.

Why is Neglecting Your Emergency Fund a Mistake?

Failing to build or replenish an emergency fund is a significant risk for any **individual**. Without this financial safety net, unexpected expenses—like a sudden job loss, medical emergency, or car repair—can quickly lead to high-interest debt, undoing months or even years of financial progress. Prioritizing the creation and maintenance of an emergency fund, ideally in a **high-yield savings account**, is a non-negotiable step for true financial security and peace of mind. It directly protects your established financial foundation.

Why is Accumulating High-Interest Debt a Critical Mistake?

Allowing **high-interest debt**, particularly from **credit cards**, to accumulate is a critical mistake. The high **interest rates** on these debts can quickly spiral out of control, making it extremely difficult to pay off the principal and often trapping **individuals** in a cycle of minimum payments. For **beginners**, learning to use credit responsibly and paying off credit card balances in full each month is paramount. If high-interest debt exists, aggressively employing strategies like the debt avalanche or snowball is essential to reduce the burden swiftly. This is a fundamental principle of sound personal finance.

Why is Delaying Investment a Costly Mistake for Beginners?

The biggest financial asset many **beginners** possess is time. Delaying **investment** means missing out on the immense power of **compound interest**. Even small, consistent investments made early in life can grow into substantial wealth over decades. The longer your money is invested, the more time it has to compound and generate returns. Procrastination in investing is a costly mistake that can significantly hinder your ability to achieve long-term financial goals, such as a comfortable retirement or financial independence. Starting early, even with small amounts, is a key recommendation from financial advisors.

Your Ongoing Journey to Personal Financial Mastery

Completing this **Personal Finance Guide for Beginners** marks not an end, but the confident beginning of your lifelong journey towards financial mastery. The principles discussed—budgeting, saving, debt management, and investing—form a dynamic framework that requires continuous engagement and adaptation. For **individuals** committed to long-term success, financial education is an ongoing process that empowers you to grow your wealth and achieve profound financial security.

Why is Continuous Learning and Adaptation Essential in Personal Finance?

The financial landscape is ever-evolving. New investment opportunities, changes in tax laws, and shifts in personal circumstances mean that **continuous learning** is essential for **beginners** to maintain and enhance their financial well-being. Regularly read reputable financial news, explore advanced investment strategies, and stay informed about economic trends. Your financial plan should be a living document, subject to periodic review and adjustment as your life stages, income, and goals evolve. This proactive approach ensures your personal finance strategies remain relevant and effective.

When Should Beginners Consider Seeking Professional Financial Guidance?

While this guide provides a strong foundation, there will be times when seeking **professional guidance** is invaluable. For complex financial decisions, such as estate planning, advanced investment strategies, or navigating significant life changes, consulting a certified financial planner or advisor can provide tailored advice. A financial professional offers expertise, an objective perspective, and can help **beginners** develop sophisticated plans to achieve ambitious financial goals, ensuring you make the most informed decisions for your unique situation. This collaboration complements your personal financial literacy, offering specialized support when you need it most.

Your journey with **personal finance** is a marathon, not a sprint. By applying the knowledge within this **Personal Finance Guide for Beginners**, consistently practicing smart money habits, and committing to continuous learning, **you** are well-positioned to achieve your financial aspirations, empower your career development, and build a life of security and abundance. Start today, stay disciplined, and watch your financial future flourish.

***

About the Author: [Author Name] is a Certified Financial Planner (CFP®) with over a decade of experience in helping individuals and families achieve their financial goals. With a passion for financial literacy, [Author Name] regularly contributes to diaalnews, sharing practical, actionable advice to empower readers on their personal finance journey. [Author Name]’s expertise includes wealth management, retirement planning, and investment strategies. Author’s Bio Page

Last Updated: September 15, 2025