Understanding Comprehensive Car Insurance: Beyond the Basics

When you invest in a vehicle, you’re not just buying a mode of transportation; you’re acquiring an asset that comes with inherent risks. While liability insurance covers damages you might cause to others and collision insurance handles repairs after an accident with another vehicle or object, comprehensive car insurance steps in to protect your vehicle from a wide array of non-collision related incidents. This often misunderstood component of an auto insurance policy is a critical layer of defense against the unexpected, offering peace of mind when Mother Nature, vandals, or even wildlife decide to interact with your car.

At its core, comprehensive coverage is designed to protect your vehicle against damages that are beyond your control and not directly related to a crash with another car or object. Think of it as an all-encompassing safety net for your automobile against the random, often unavoidable misfortunes that can befall it. Unlike collision coverage, which focuses on impacts, comprehensive coverage casts a wider net, addressing external threats that can result in significant financial loss if you’re left to cover the costs out-of-pocket. This distinction is crucial, particularly for those who own newer, more valuable vehicles, or live in areas prone to specific environmental hazards.

Many drivers mistakenly believe that having liability and collision is enough, but overlooking comprehensive insurance can leave gaping holes in your financial protection. Imagine waking up to find your car stolen, or returning to your parking spot only to discover a massive tree branch has fallen directly onto your roof during a storm. Without comprehensive coverage, these scenarios could lead to substantial repair bills or the complete loss of your vehicle’s value, forcing you to bear the entire financial burden. In an economic climate where every dollar counts, such an unexpected expense can derail even the most carefully constructed personal budget. Therefore, understanding what this coverage entails is not just about insurance literacy; it’s about practical financial resilience.

The landscape of insurance, much like the broader economic and political environment, is constantly evolving. Just as discussions around how the new administration will impact health coverage for Americans highlight the need for citizens to stay informed about policy changes affecting their well-being, vehicle owners must similarly remain vigilant about their auto insurance policies. What was sufficient a few years ago might not adequately protect you in 2026, especially with advancements in vehicle technology and changing risk profiles. Comprehensive coverage, therefore, is not a static product but a dynamic shield that requires periodic review to ensure it aligns with your current assets, lifestyle, and potential risks.

Core Protections: What Comprehensive Coverage Typically Includes

The beauty of comprehensive car insurance lies in its versatility, covering a multitude of perils that collision or liability policies do not. While specific coverages can vary slightly between providers and regions, there’s a consistent set of core protections that typically fall under the comprehensive umbrella. Understanding these specific scenarios is key to appreciating the value comprehensive insurance brings to your financial planning.

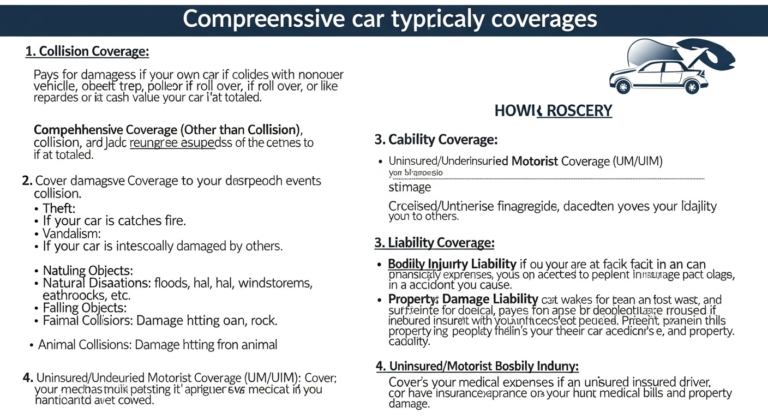

1. Theft and Vandalism

One of the most common and devastating non-collision incidents is the theft of your vehicle or damage sustained due to vandalism. Comprehensive insurance provides coverage if your car is stolen and not recovered, or if it is recovered but damaged. It also covers damages resulting from malicious acts, such as slashed tires, broken windows, keying, or other intentional harm inflicted upon your vehicle. This protection is invaluable, especially in urban areas or for vehicles that are frequently parked in public spaces, offering a crucial safety net against criminal activity.

2. Fire Damage

From engine fires to arson, fire can quickly decimate a vehicle, rendering it a total loss. Comprehensive coverage steps in to cover the costs of repairs or the actual cash value of your car if it’s damaged or destroyed by fire. This protection extends beyond just accidental fires; if your car is set ablaze intentionally by someone else, comprehensive insurance will still cover the resulting damage, providing a critical financial buffer against catastrophic loss.

3. Natural Disasters and Environmental Damage

Mother Nature can be unpredictable, and her wrath can take many forms that pose a threat to your vehicle. Comprehensive insurance is your primary defense against a wide range of natural disasters, including:

- Hail: Hailstorms can cause significant dents and damage to your car’s exterior, windshield, and windows. Comprehensive coverage will pay for the repairs.

- Floods: Water damage, especially from floods, can be incredibly destructive to a car’s engine, interior, and electrical systems. Comprehensive policies typically cover flood-related damage.

- Windstorms: High winds can cause debris to strike your car, or even blow your vehicle into another object. Damages from wind, including those from tornados and hurricanes, are generally covered.

- Earthquakes: While less common in some regions, earthquakes can cause vehicles to be damaged by falling structures or to shift and collide with other objects. Comprehensive insurance covers these specific damages.

- Falling Objects: This is a broad category that includes anything from tree branches falling onto your car during a storm, to rocks or other debris kicked up by trucks, or even items falling from construction sites.

4. Animal Collisions

Hitting an animal on the road, particularly larger ones like deer or elk, can cause significant damage to your vehicle and pose a serious safety risk. While it involves a collision, striking an animal is typically covered under comprehensive insurance, not collision coverage, because it’s considered an uncontrollable event. This distinction is important for understanding how your policy will respond in such an incident.

5. Glass Breakage

Your vehicle’s glass components – windshield, side windows, and rear window – are highly susceptible to damage from various sources, such as flying rocks or vandalism. Comprehensive coverage typically includes protection for glass breakage, often with a lower or even no deductible in some policies, recognizing the frequency and necessity of such repairs for safe driving.

Each of these protections underscores the value of comprehensive car insurance as a multi-faceted shield. Without it, the financial burden of these common, yet often unavoidable, incidents would fall entirely on the vehicle owner. In a year like 2026, where economic stability remains a key concern for many households, having such a robust safety net for your vehicle becomes not just a convenience, but a financial imperative.

Add-Ons and Enhancements: Tailoring Your Policy for 2026

1. Rental Car Reimbursement

If your car is damaged due to a covered comprehensive claim (e.g., theft, fire, natural disaster) and needs repairs, this add-on covers the cost of a rental car for a specified period. This is incredibly useful, as it ensures you retain mobility and don’t incur additional transportation costs while your primary vehicle is out of commission. It’s a practical enhancement that minimizes disruption to your daily life.

2. Towing and Labor Coverage

This endorsement helps cover the cost of towing your vehicle to a repair shop if it breaks down or is rendered inoperable due to a covered incident, and it often includes roadside assistance for minor repairs like jump-starts, tire changes, or fuel delivery. While not strictly a comprehensive add-on in some policies, it often complements the peace of mind offered by comprehensive coverage by addressing non-accident related vehicle emergencies.

3. Custom Parts and Equipment Coverage

If you’ve invested in aftermarket modifications for your vehicle, such as custom rims, a high-end sound system, performance upgrades, or specialized accessories, standard comprehensive coverage might not fully cover their replacement value. This add-on specifically covers the cost of repairing or replacing these custom parts and equipment if they are damaged or stolen in a covered comprehensive event, ensuring your investment is fully protected.

4. Gap Insurance

For those who finance or lease a new vehicle, gap insurance is a critical consideration. In the event of a total loss (e.g., your car is stolen and not recovered, or destroyed by fire), your comprehensive policy will typically pay out the actual cash value (ACV) of your vehicle at the time of loss. If you owe more on your loan or lease than the car’s ACV, gap insurance covers the “gap” between what you owe and what your comprehensive policy pays, preventing you from being upside down on your loan. This is particularly relevant for newer vehicles that depreciate quickly.

5. New Car Replacement Coverage

Similar to gap insurance but offering different protection, new car replacement coverage, if available, ensures that if your relatively new vehicle is totaled within a certain timeframe (e.g., the first year or two of ownership), your insurer will pay for a brand-new car of the same make and model, rather than just its depreciated actual cash value. This can be a significant benefit for owners of new cars, protecting against the immediate depreciation hit.

The decision to include these add-ons depends heavily on your individual circumstances, the value of your vehicle, and your risk tolerance. Much like the broader policy discussions surrounding public services and individual protections, such as how the new administration will impact health coverage for Americans, the world of car insurance is not static. Policies and available enhancements evolve, and what was considered standard protection years ago might now be supplemented by more specialized options. It’s imperative for consumers in 2026 to regularly review their insurance needs, ensuring their policy remains aligned with their current assets and financial goals. A proactive approach to understanding and customizing your comprehensive coverage can save you considerable stress and financial outlay in the long run.

The Difference: Comprehensive vs. Collision vs. Liability

To truly grasp the importance of comprehensive car insurance, it’s essential to understand how it differs from the other primary types of auto coverage: collision and liability. These three components often work in conjunction to provide a full spectrum of protection, but each addresses distinct scenarios. Confusing them can lead to significant gaps in your coverage or unnecessary expenses.

1. Liability Insurance: Protecting Others

Liability insurance is arguably the most fundamental type of auto insurance, and it is legally mandated in most states and countries. Its primary purpose is to cover damages and injuries you cause to other people and their property in an at-fault accident. It typically has two main components:

- Bodily Injury Liability: Covers medical expenses, lost wages, and pain and suffering for anyone injured in an accident you cause.

- Property Damage Liability: Covers the cost of repairing or replacing property (like another vehicle, a fence, or a building) that you damage in an accident.

Crucially, liability insurance does not cover damages to your own vehicle or your own medical expenses. It is solely focused on compensating third parties for damages you are responsible for.

2. Collision Insurance: Protecting Your Vehicle from Accidents

Collision insurance covers the cost of repairing or replacing your own vehicle if it is damaged in an accident, regardless of who is at fault. This includes hitting another car, colliding with a stationary object (like a tree, pole, or guardrail), or even rolling your vehicle. If you lease or finance your car, collision coverage is almost always required by the lender. It’s designed to restore your vehicle to its pre-accident condition or pay out its actual cash value if it’s deemed a total loss. Unlike liability, collision coverage is optional once your car is paid off, but it’s highly recommended for vehicles with significant value.

3. Comprehensive Insurance: Protecting Your Vehicle from Non-Collision Perils

As we’ve extensively covered, comprehensive car insurance protects your vehicle from damages that are not caused by a collision with another vehicle or object. It covers incidents like theft, vandalism, fire, natural disasters (hail, flood, wind, earthquakes), falling objects, and animal collisions. Like collision coverage, it is typically optional unless required by a lender. Comprehensive coverage is paid out regardless of who is at fault, as these incidents are generally considered beyond human control (with the exception of vandalism or theft).

To illustrate the distinctions, consider these scenarios:

- If you rear-end another car at a stop sign: Your liability insurance would cover the damages to the other car and injuries to its occupants. Your collision insurance would cover the damages to your own vehicle. Comprehensive insurance would not apply.

- If your car is stolen from your driveway overnight: Your comprehensive insurance would cover the loss of your vehicle. Collision and liability insurance would not apply.

- If a tree falls on your parked car during a storm: Your comprehensive insurance would cover the damage to your vehicle. Collision and liability insurance would not apply.

Understanding these distinct roles is vital for making an informed decision about your auto insurance package. While liability is mandatory for protecting others, comprehensive and collision coverage are essential for protecting your own financial investment in your vehicle. For many, especially those with newer or more valuable cars, carrying all three provides the most robust financial protection against a wide range of unforeseen circumstances. Deciding which combination is right for you in 2026 requires a careful assessment of your vehicle’s value, your financial situation, and your risk tolerance, echoing the thoroughness needed when answering the broader question of how do you know which insurance plan is right for you in any aspect of life.

Factors Influencing Your Comprehensive Premium and Smart Savings

The cost of comprehensive car insurance isn’t a fixed figure; it’s a dynamic calculation influenced by a multitude of factors. Understanding these variables can empower you to make informed choices that could potentially lower your premiums while still maintaining robust coverage. In 2026, as economic pressures and insurance market dynamics continue to shift, optimizing your premium is more important than ever.

1. Your Vehicle’s Make, Model, and Age

The type of car you drive significantly impacts your comprehensive premium. Insurers assess the likelihood of a vehicle being stolen, its susceptibility to damage (e.g., glass breakage, ease of repair), and the cost of parts. Luxury cars, sports cars, and certain models known for being theft targets often command higher comprehensive premiums. Newer vehicles, with their higher actual cash value, also typically have higher comprehensive costs compared to older, less valuable cars.

2. Your Location

Where you live and park your car plays a crucial role. Urban areas with higher rates of theft, vandalism, or natural disaster occurrences (like hailstorms or floods) often have higher comprehensive premiums. Conversely, living in a rural area with lower crime rates and fewer environmental risks might result in lower costs. Even specific neighborhoods within the same city can have differing rates based on claims history.

3. Your Deductible Choice

The deductible is the amount of money you agree to pay out-of-pocket before your insurance coverage kicks in. Choosing a higher deductible (e.g., $1,000 instead of $500) will generally lower your comprehensive premium because you’re taking on more of the initial financial risk. However, it’s crucial to select a deductible you can comfortably afford in the event of a claim.

4. Your Driving Record and Claims History

While comprehensive claims are often for events beyond your control, a history of frequent claims, regardless of type, can sometimes influence an insurer’s perception of your overall risk profile. A clean driving record (absence of accidents or tickets) generally contributes to lower overall insurance costs, including comprehensive.

5. Your Age and Experience

Statistically, younger, less experienced drivers are often considered higher risk by insurers across all types of coverage, including comprehensive. This is due to a higher propensity for accidents and, in some cases, a higher likelihood of vehicle theft or damage. This is a common challenge globally, and we see specific advice tailored to this demographic. For instance, 3 car insurance tips for young people in Australia 2 often include suggestions like choosing a safer car model, maintaining a good driving record, and opting for higher deductibles to manage premiums. While these tips are specific to Australia, the underlying principles apply universally: responsible driving and strategic policy choices can mitigate costs for young drivers everywhere.

6. Anti-Theft and Safety Devices

Installing anti-theft devices (e.g., car alarms, tracking systems, immobilizers) can lead to discounts on your comprehensive premium. Insurers view these as effective deterrents to theft, reducing their potential payout. Similarly, vehicles equipped with advanced safety features might also qualify for other discounts that can indirectly impact your overall policy cost.

7. Bundling Policies and Discounts

Most insurance companies offer discounts for bundling multiple policies (e.g., auto and home insurance) with the same provider. Other common discounts include multi-car discounts, good student discounts (for young drivers), low mileage discounts, and loyalty discounts. Always inquire about all available discounts to maximize your savings.

By understanding these factors and actively seeking ways to mitigate risk and qualify for discounts, vehicle owners in 2026 can effectively manage their comprehensive car insurance costs. It’s not just about finding the cheapest policy, but finding the most cost-effective one that provides adequate protection for your specific needs, aligning with the broader philosophy of smart financial planning.

Making the Right Choice: How Do You Know Which Insurance Plan Is Right For You?

Choosing the right comprehensive car insurance plan is not a one-size-fits-all decision. It requires a thoughtful evaluation of your personal circumstances, your vehicle’s value, your financial health, and your tolerance for risk. This process is akin to selecting any major financial product – whether it’s a mortgage, an investment portfolio, or even health coverage. The question of how do you know which insurance plan is right for you is central to making an informed decision that truly protects your assets without overextending your budget in 2026.

1. Assess Your Vehicle’s Value

The first step is to determine the actual cash value (ACV) of your vehicle. If your car is older and its market value is low, the cost of comprehensive coverage might outweigh the potential payout after a deductible. For instance, if your car is worth $2,000 and your comprehensive deductible is $1,000, you might only receive $1,000 in a claim. Consider if this level of protection is worth the annual premium. Conversely, if you own a new or high-value vehicle, comprehensive coverage is almost always a wise investment to protect a significant asset.

2. Evaluate Your Financial Situation and Risk Tolerance

Can you afford to replace your car out-of-pocket if it’s stolen or totaled by a natural disaster? If the answer is no, comprehensive coverage is likely essential. Your risk tolerance also plays a role: are you comfortable taking on the financial risk of a potential loss, or do you prefer the peace of mind that comes with knowing your insurer will cover non-collision damages? Your budget will also dictate your deductible choice; opt for a higher deductible to lower premiums only if you have sufficient emergency savings to cover that deductible.

3. Consider Your Driving Habits and Environment

Do you park your car in a secure garage or on a busy street? Do you live in an area prone to severe weather (hail, floods) or high crime rates? Your environment and parking habits directly influence the likelihood of comprehensive claims. If you’re in a high-risk area, comprehensive coverage becomes even more critical.

4. Understand Lender Requirements

If you have a loan or lease on your vehicle, your lender will almost certainly require you to carry comprehensive (and collision) insurance until the loan is paid off. Failing to do so can result in forced-placed insurance, which is often more expensive and offers less coverage.

5. Compare Quotes from Multiple Providers

Never settle for the first quote you receive. Insurance rates can vary significantly between companies for the exact same coverage. Obtain quotes from at least three to five different insurers, comparing not just the price but also the coverage limits, deductibles, available add-ons, and the company’s customer service reputation. Utilize online comparison tools and consider working with an independent insurance agent who can shop around on your behalf.

6. Read the Fine Print

Before committing to any policy, thoroughly read the policy documents. Understand what is covered, what is excluded, the claims process, and any limitations or specific conditions. Don’t hesitate to ask your agent or insurer for clarification on anything you don’t understand. This diligence is paramount across all forms of insurance, whether it’s understanding the nuances of how the new administration will impact health coverage for Americans or deciphering the specifics of your auto policy.

7. Re-evaluate Periodically

Your life circumstances change, and so should your insurance policy. Review your comprehensive coverage annually or whenever you experience a significant life event, such as buying a new car, moving, getting married, or when your financial situation changes. What was right for you last year might not be the optimal choice in 2026.

Ultimately, choosing the right comprehensive car insurance plan is about finding the sweet spot between adequate protection and affordability. It’s a key component of a sound financial strategy, ensuring that your vehicle remains protected against the many non-collision threats it faces, allowing you to drive with greater confidence and peace of mind.

Navigating Claims and Maximizing Your Comprehensive Coverage

Understanding what comprehensive car insurance covers is only half the battle; knowing how to navigate the claims process effectively is equally crucial. When an unfortunate incident occurs, being prepared can make a significant difference in how smoothly and successfully your claim is processed, ensuring you maximize the benefits of your comprehensive coverage.

1. Act Promptly After an Incident

As soon as it is safe to do so, report the incident to your insurance company. Most insurers have a claims hotline available 24/7 or an online portal for reporting. Timely reporting is essential, as delays can sometimes complicate the claims process or raise questions about the extent of the damage. For instance, if your car is stolen, contact the police immediately to file a report, and then notify your insurer with the police report number.

2. Document Everything

Comprehensive claims often involve damage from external sources. Detailed documentation is your best friend. Take clear photos and videos of the damage, the surrounding area, and any contributing factors (e.g., fallen tree, floodwaters, vandalism). If there are witnesses, collect their contact information. For theft, provide your insurer with all relevant vehicle information, including VIN, license plate number, and any tracking device details. The more evidence you can provide, the stronger your claim will be.

3. Prevent Further Damage

After an incident, take reasonable steps to prevent further damage to your vehicle. For example, if a window is broken, cover it to protect the interior from rain or theft. If your car has sustained flood damage, do not attempt to start it, as this could cause further mechanical issues. Your policy usually requires you to mitigate further loss, and insurers appreciate proactive measures.

4. Understand Your Policy and Deductible

Before the claims process begins in earnest, review your policy documents to understand your comprehensive coverage limits, exclusions, and, most importantly, your deductible. Knowing your deductible amount ensures you’re prepared for your out-of-pocket expense. If the cost of repairs is less than your deductible, it might not be worth filing a claim, as it could still be recorded on your claims history.

5. Cooperate with Your Adjuster

6. Get Repair Estimates

While your insurer might recommend specific repair shops, you generally have the right to choose where your vehicle is repaired. Obtain at least one, and preferably two, detailed repair estimates from reputable mechanics. Compare these estimates with the adjuster’s assessment. If there’s a significant discrepancy, discuss it with your adjuster to ensure all necessary repairs are covered.

7. Review the Settlement Offer

Navigating an insurance claim can be stressful, but by understanding the process and acting diligently, you can ensure that your comprehensive car insurance serves its purpose effectively. In 2026, with the increasing sophistication of vehicle technology and the potential for higher repair costs, maximizing your coverage means not just having the right policy, but also knowing how to leverage it when you need it most.

FAQ: Comprehensive Car Insurance Explained

What is the primary difference between comprehensive and collision coverage?

Comprehensive coverage protects your vehicle from damages not caused by a collision, such as theft, vandalism, fire, natural disasters, falling objects, and animal collisions. Collision coverage, on the other hand, pays for damages to your own vehicle resulting from an accident with another vehicle or object, regardless of who is at fault. Both are designed to protect your vehicle but cover different types of incidents.

Is comprehensive car insurance mandatory?

Generally, comprehensive car insurance is not legally mandated by state or federal law. However, if you have a loan or lease on your vehicle, your lender will almost certainly require you to carry both comprehensive and collision insurance until the debt is paid off. Once your car is fully owned, comprehensive coverage becomes optional, though highly recommended for financial protection.

Does comprehensive insurance cover hail damage?

Yes, comprehensive car insurance typically covers damage to your vehicle caused by hail. This falls under the category of natural disasters and environmental damage, which is a core protection offered by comprehensive policies. This includes dents to the body, broken glass, or other structural damage resulting from hailstorms.

Will my comprehensive premium increase if I file a claim?

While comprehensive claims are often for events beyond your control (like weather or theft), filing a claim can sometimes lead to an increase in your premium upon renewal. Insurers assess risk based on various factors, including claims history. However, a single comprehensive claim might have less impact than an at-fault collision claim. The specific impact can vary by insurer and your overall claims history.

What is a deductible, and how does it relate to comprehensive coverage?

A deductible is the amount of money you agree to pay out-of-pocket towards a covered loss before your insurance company starts to pay. For comprehensive coverage, if you have a $500 deductible and your car sustains $2,000 in covered damage, you would pay the first $500, and your insurer would pay the remaining $1,500. Choosing a higher deductible usually results in lower premiums, but means a larger out-of-pocket expense if you file a claim.

Does comprehensive insurance cover mechanical breakdown?

No, comprehensive car insurance does not cover mechanical breakdowns, wear and tear, or general maintenance issues. Its focus is on damage caused by non-collision external events. For mechanical issues, you would typically need a separate extended warranty or mechanical breakdown insurance, which is a different product entirely from standard auto insurance.

Recommended Resources

Learn more about this topic in Automotive Lightweighting Materials at Mitsubishi Manufacturing.

Explore Child Tax Credit Explained for additional insights.