How to Start Investing: Your Comprehensive Guide to Building Wealth in 2026

Affiliate disclosure: This article may contain affiliate links. Recommendations are independent and editorially driven.

The journey to financial independence often begins with a single, crucial step: learning how to start investing. For many, the world of investing seems complex, intimidating, and reserved for financial gurus. However, in 2026, with an abundance of accessible platforms, educational resources, and diverse investment vehicles, there has never been a better time for individuals from all walks of life to begin building their wealth.

Investing isn’t just about accumulating money; it’s about making your money work for you, harnessing the power of compound interest, and achieving long-term financial goals, whether that’s buying a home, funding your children’s education, or securing a comfortable retirement. This comprehensive guide will demystify the process, breaking down everything you need to know about how to start investing, from foundational principles to advanced strategies.

We’ll walk you through assessing your financial readiness, setting realistic goals, understanding different investment types, managing risk, and choosing the right platforms. By the end of this guide, you’ll have a clear roadmap and the confidence to take your first steps into the exciting world of investing, transforming your financial future.

Understanding the Basics: Why Investing Matters

Before diving into the mechanics of how to start investing, it’s crucial to grasp the fundamental ‘why.’ Investing isn’t a get-rich-quick scheme; it’s a long-term strategy designed to grow your capital over time, outpacing inflation and building substantial wealth. Here’s why it’s a cornerstone of sound financial planning:

The Power of Compounding: Your Money’s Best Friend

Compound interest is often called the “eighth wonder of the world.” It’s the process where the returns on your investments are reinvested, generating their own returns. Over time, this creates an exponential growth effect. Imagine you invest $1,000 and earn 7% in the first year. You now have $1,070. In the second year, you earn 7% on $1,070, not just your original $1,000. This snowball effect is why starting early is paramount. Even small, consistent investments can accumulate into significant wealth over decades.

Beating Inflation: Protecting Your Purchasing Power

Inflation is the silent assassin of savings. It’s the rate at which the general level of prices for goods and services is rising, and consequently, the purchasing power of currency is falling. If your money is just sitting in a standard savings account earning a negligible interest rate, its real value is eroding year after year. Investing, particularly in assets that historically outperform inflation like stocks or real estate, helps your money retain and even grow its purchasing power, ensuring your future self can afford more, not less.

Achieving Financial Goals: From Retirement to Education

Specific financial goals often require substantial capital. Whether it’s a down payment on a house, funding a child’s college education, or securing a comfortable retirement, saving alone often isn’t enough. Investing provides the accelerated growth needed to reach these milestones. By aligning your investment strategy with your goals, you can calculate the approximate amount you need to invest regularly and the expected rate of return to hit your targets within a desired timeframe.

Diversification and Risk Mitigation Over Time

While investing always carries some risk, a well-diversified portfolio can mitigate specific risks. Spreading your investments across various asset classes, industries, and geographies reduces the impact of a poor performance by any single investment. Furthermore, over long periods, market fluctuations tend to smooth out, making long-term investing generally less risky than short-term trading.

[INLINE IMAGE 1: place after second H2 | alt=”how to start investing concept illustration”]

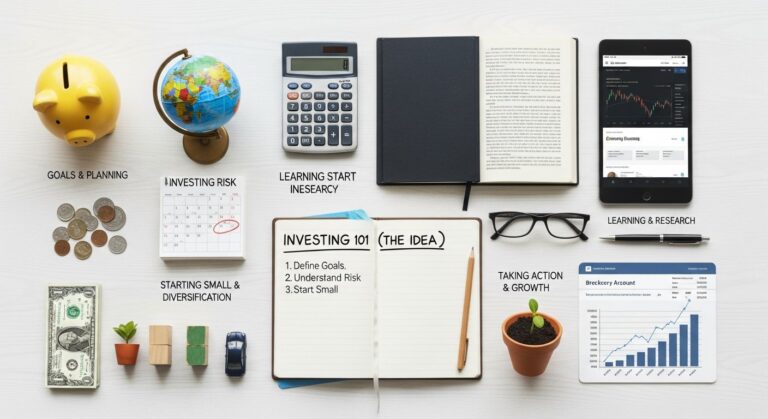

Assessing Your Financial Readiness: The Pre-Investment Checklist

Before you even think about opening a brokerage account, it’s essential to ensure your personal finances are in order. Skipping these crucial preliminary steps can lead to unnecessary stress and potentially jeopardize your investments.

1. Clear Your High-Interest Debt

This is arguably the most critical step. High-interest debt, such as credit card balances or personal loans, can carry annual interest rates of 15% to 25% or even higher. It’s extremely difficult for investments to consistently generate returns high enough to outpace these costs. Paying off high-interest debt offers a guaranteed “return” equal to the interest rate you avoid paying, making it a powerful first investment in itself. Focus on a debt repayment strategy, like the snowball or avalanche method, before allocating significant funds to investments.

2. Build a Robust Emergency Fund

Life is unpredictable, and unexpected expenses can derail your financial plans. An emergency fund is a readily accessible savings account holding 3 to 6 months’ worth of essential living expenses. This fund acts as a financial safety net, preventing you from having to sell investments prematurely (potentially at a loss) or incur new debt when faced with job loss, medical emergencies, or car repairs. This fund should be liquid, meaning it’s easy to access, typically in a high-yield savings account.

3. Understand Your Monthly Budget and Cash Flow

You can’t effectively invest if you don’t know where your money is going. Creating a detailed monthly budget allows you to track income and expenses, identify areas for savings, and determine how much money you can realistically allocate to investing each month without straining your finances. Knowing your cash flow helps you make consistent contributions, which is key to long-term investment success.

- Track Income: List all sources of income.

- Track Expenses: Categorize fixed (rent, loan payments) and variable (groceries, entertainment) expenses.

- Identify Savings Opportunities: Look for areas to reduce spending and redirect those funds to your investment portfolio.

4. Define Your Investment Capital

Once high-interest debt is managed and your emergency fund is robust, determine how much money you can comfortably set aside for investing on a regular basis. This doesn’t have to be a large sum to start. Many platforms allow you to begin investing with as little as $50 or $100 per month. The key is consistency. Even small, regular contributions can grow substantially over time due to compounding.

Setting Your Investment Goals and Time Horizon

Knowing why you’re investing is just as important as knowing how to start investing. Your goals will dictate your investment strategy, risk tolerance, and the types of assets you choose.

Short-Term Goals (1-5 Years)

These goals typically include saving for a down payment on a car, a vacation, or a small home renovation. For short-term goals, capital preservation and liquidity are more important than aggressive growth.

- Investment Focus: Low-risk, highly liquid assets.

- Examples: High-yield savings accounts, Certificates of Deposit (CDs), money market accounts, short-term bond funds.

- Risk Tolerance: Very low. You cannot afford significant fluctuations.

Medium-Term Goals (5-15 Years)

These might include saving for a child’s college education, a larger home down payment, or starting a business. With a slightly longer time horizon, you can afford to take on a bit more risk for potentially higher returns.

- Investment Focus: A balanced approach between growth and stability.

- Examples: Diversified portfolios including a mix of stocks (through ETFs or mutual funds) and bonds.

- Risk Tolerance: Moderate. You have time to recover from minor market downturns.

Long-Term Goals (15+ Years)

Retirement savings is the quintessential long-term goal. With decades ahead, you can embrace more risk for maximum growth potential.

- Investment Focus: Growth-oriented assets.

- Examples: Predominantly equities (stocks, stock ETFs, growth mutual funds), potentially some real estate or alternative investments as you become more experienced.

- Risk Tolerance: High to moderate. Market volatility over short periods is less concerning as you have ample time for recovery.

Matching Goals to Your Investment Horizon

It’s crucial to align your investment horizon with the types of investments you choose. Attempting to achieve short-term goals with volatile, long-term assets can lead to losses if you need to liquidate during a market downturn. Conversely, using conservative, short-term instruments for long-term goals might leave you short of your target due to insufficient growth. This step is fundamental to a successful strategy when learning how to start investing.

Understanding Risk and Your Risk Tolerance

Risk is an inherent part of investing. There’s no such thing as a risk-free investment that offers significant returns. However, understanding different types of risk and your personal tolerance for it is paramount before you begin investing.

What is Investment Risk?

Investment risk refers to the probability or likelihood of an actual return being different from the expected return. This includes the possibility of losing some or all of your initial investment. Common types of risk include:

- Market Risk: The risk that the entire market or a specific sector will decline, impacting your investments regardless of their individual performance.

- Inflation Risk: The risk that inflation will erode the purchasing power of your investment returns.

- Interest Rate Risk: The risk that changes in interest rates will negatively affect the value of fixed-income investments like bonds.

- Liquidity Risk: The risk that you may not be able to sell an investment quickly enough at a fair market price (e.g., real estate vs. publicly traded stocks).

- Credit Risk: The risk that a bond issuer will default on its payments (relevant for bondholders).

Assessing Your Personal Risk Tolerance

Your risk tolerance is your willingness and ability to take on financial risk. It’s influenced by several factors:

- Time Horizon: As discussed, longer horizons generally allow for higher risk.

- Financial Stability: A robust emergency fund and stable income allow for greater risk.

- Personality and Emotions: How will you react to market downturns? Can you stomach watching your portfolio temporarily lose value without panic-selling?

- Investment Knowledge: Greater understanding often leads to more comfortable risk-taking.

Many online brokerage platforms and financial advisors offer risk assessment questionnaires designed to help you quantify your tolerance. Be honest with yourself. It’s better to start conservatively and gradually increase your risk exposure as you gain experience and comfort, rather than taking on too much risk and making impulsive decisions during market volatility.

Understanding market volatility and how to manage it is a key aspect of building a resilient investment strategy.

Exploring Investment Vehicles: Where to Put Your Money

Once you’ve prepared your finances and set your goals, the next step in how to start investing is to understand the various investment vehicles available. Each comes with its own risk-reward profile and is suitable for different goals.

1. Stocks (Equities)

When you buy a stock, you’re purchasing a small piece of ownership in a public company. As the company grows and profits, the value of its stock can increase, and you might receive dividends (a portion of the company’s earnings).

- Pros: High growth potential over the long term; ownership in successful companies.

- Cons: High volatility; individual stocks can be risky; requires research.

- Best For: Long-term growth, higher risk tolerance.

2. Bonds (Fixed Income)

Bonds are essentially loans you make to governments or corporations. In return, the issuer promises to pay you regular interest payments and return your principal investment at a specified maturity date.

- Pros: Generally less volatile than stocks; provides regular income; good for capital preservation.

- Cons: Lower growth potential than stocks; susceptible to interest rate risk.

- Best For: Capital preservation, income generation, lower risk tolerance, diversifying a portfolio.

3. Mutual Funds

A mutual fund is a professionally managed portfolio that pools money from many investors to purchase a diverse collection of stocks, bonds, or other securities.

- Pros: Instant diversification; professional management; convenient.

- Cons: Management fees (expense ratios) can eat into returns; lack of control over individual holdings.

- Best For: Beginners seeking diversification and professional management without picking individual securities.

4. Exchange-Traded Funds (ETFs)

ETFs are similar to mutual funds in that they hold a basket of securities, but they trade on stock exchanges throughout the day like individual stocks. They often track an index (e.g., S&P 500), a sector, or a commodity.

- Pros: Diversification; typically lower expense ratios than actively managed mutual funds; flexibility to trade throughout the day.

- Cons: Trading fees (though many brokers offer commission-free ETF trading); market price can differ slightly from net asset value.

- Best For: Cost-effective diversification, broad market exposure, suitable for all risk tolerances depending on the ETF’s holdings.

5. Real Estate

Investing in real estate can involve buying physical properties (residential, commercial), Real Estate Investment Trusts (REITs), or real estate crowdfunding.

- Pros: Potential for capital appreciation and rental income; tangible asset.

- Cons: Illiquid; high upfront costs (for physical property); management responsibilities.

- Best For: Long-term investors, those with significant capital or seeking diversification beyond traditional securities. REITs offer a more liquid way to invest in real estate.

6. Certificates of Deposit (CDs)

CDs are savings certificates with a fixed maturity date and a fixed interest rate. You deposit a sum of money for a set period, and the bank pays you interest.

- Pros: Very low risk; predictable returns; FDIC-insured up to certain limits.

- Cons: Lower returns; funds are locked in for the term (though penalties for early withdrawal exist).

- Best For: Short-term savings goals, emergency fund overflow, very low risk tolerance.

7. Cryptocurrencies (e.g., Bitcoin, Ethereum)

Digital or virtual currencies that use cryptography for security and operate independently of a central bank.

- Pros: Potentially very high returns; innovative technology.

- Cons: Extremely volatile; largely unregulated; complex to understand; susceptible to scams and hacks.

- Best For: Investors with a very high risk tolerance, comfortable with significant fluctuations, and only with a small portion of their overall portfolio.

[INLINE IMAGE 2: place after fourth H2 | alt=”how to start investing comparison illustration”]

Here’s a comparison table summarizing some key characteristics of popular investment vehicles:

| Investment Type | Primary Benefit | Typical Risk Level | Liquidity | Minimum Investment (approx.) |

|---|---|---|---|---|

| Individual Stocks | High Growth Potential | High | High | Cost of one share (e.g., $50-$500+) |

| Bonds | Income, Stability | Low to Moderate | Moderate to High | $1,000+ (individual), lower for bond funds |

| Mutual Funds | Diversification, Professional Management | Moderate | Moderate (daily trading) | $500-$3,000+ (initial) |

| Exchange-Traded Funds (ETFs) | Diversification, Low Cost, Flexibility | Low to High (depends on holdings) | High (intra-day trading) | Cost of one share (e.g., $20-$300+) |

| Real Estate (REITs) | Income, Growth, Inflation Hedge | Moderate | High (REITs) | Cost of one REIT share (e.g., $50-$200+) |

| Certificates of Deposit (CDs) | Guaranteed Returns, Capital Preservation | Very Low | Low (funds locked) | $500-$1,000+ |

Choosing the Right Investment Accounts and Platforms

Once you know what you want to invest in, you need a place to do it. The type of account and platform you choose can significantly impact your investment journey. When considering how to start investing, this step is more practical than theoretical.

Types of Investment Accounts

The account you choose will determine tax implications, contribution limits, and how you access your money.

- Taxable Brokerage Accounts:

- Description: Standard investment accounts where you pay taxes on capital gains, dividends, and interest each year. No contribution limits, great flexibility.

- Best For: Short-term goals, accessible funds, investing beyond retirement limits.

- Tax-Advantaged Retirement Accounts: These are crucial for long-term wealth building due to their tax benefits.

- 401(k) or 403(b): Employer-sponsored plans. Contributions are often pre-tax (reducing current taxable income), and growth is tax-deferred until retirement. Many employers offer matching contributions, which is essentially free money.

- Individual Retirement Accounts (IRAs):

- Traditional IRA: Contributions may be tax-deductible, and growth is tax-deferred. Withdrawals in retirement are taxed as ordinary income.

- Roth IRA: Contributions are made with after-tax money, but qualified withdrawals in retirement are completely tax-free. Excellent for those who expect to be in a higher tax bracket in retirement.

- Health Savings Account (HSA): If you have a high-deductible health plan, an HSA offers a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. It can also function as a supplemental retirement account after age 65.

- 529 Plans:

- Description: Tax-advantaged savings plans designed to encourage saving for future education costs. Earnings grow tax-free, and withdrawals for qualified educational expenses are also tax-free.

- Best For: Saving for college or vocational training.

Choosing an Investment Platform or Brokerage

With numerous online brokers available, consider these factors:

- Fees and Commissions: Look for commission-free stock and ETF trades. Be aware of expense ratios for mutual funds, account maintenance fees, or inactivity fees.

- Minimum Investment: Some platforms allow you to start with very little, offering fractional shares, while others have higher minimums for certain funds or accounts.

- Investment Options: Does the platform offer the types of investments you’re interested in (stocks, ETFs, mutual funds, bonds, crypto)?

- Tools and Resources: Look for robust research tools, educational content, portfolio analysis, and goal-setting features.

- User Experience: Is the platform intuitive and easy to navigate for beginners? Do they have a mobile app?

- Customer Support: Are they responsive and helpful?

Popular online brokerage options for beginners in 2026 often include:

- Fidelity: Known for low-cost index funds, robust research, and excellent customer service.

- Charles Schwab: Offers a wide range of investment products, low fees, and strong customer support.

- Vanguard: Famous for its low-cost index funds and ETFs, ideal for long-term passive investors.

- E*TRADE: A well-established platform with a good balance of features for beginners and experienced traders.

- Robinhood: Popular for its user-friendly interface and commission-free trading, though sometimes criticized for encouraging speculative trading.

- M1 Finance: Combines automated investing with customization, allowing you to build “pies” of investments.

- Robo-Advisors (e.g., Betterment, Wealthfront): Offer automated portfolio management based on your goals and risk tolerance, with very low minimums and management fees. They’re an excellent option for hands-off investing.

Finding the best brokerage account for beginners can significantly simplify your entry into investing.

Starting Your Investment Journey: Practical Strategies for Beginners

Once you’ve done your homework and chosen your platform, it’s time to put your plan into action. Here are some practical strategies for how to start investing effectively as a beginner.

1. Start Small and Stay Consistent

You don’t need a fortune to begin investing. Many platforms allow you to start with as little as $50 or $100. The key is to make investing a regular habit. Automate your investments if possible, setting up recurring transfers from your checking account to your investment account. This consistency, combined with compounding, is far more powerful than trying to time the market with large, infrequent contributions.

2. Embrace Diversification

The old adage “don’t put all your eggs in one basket” is particularly true for investing. Diversification means spreading your investments across different asset classes (stocks, bonds, real estate), industries, and geographical regions. This strategy reduces risk because if one investment performs poorly, others may perform well, cushioning the impact on your overall portfolio.

- Example: Instead of buying stock in just one tech company, invest in an S&P 500 index ETF, which gives you exposure to 500 of the largest U.S. companies across various sectors.

3. Consider Index Funds and ETFs (Exchange-Traded Funds)

For most beginners, individual stock picking is too risky and time-consuming. Index funds and ETFs are excellent alternatives because they offer instant diversification at a low cost.

- Index Funds: These funds passively track a specific market index (e.g., S&P 500, NASDAQ, total stock market). They aim to match the performance of the index, not beat it, and typically have very low expense ratios.

- ETFs: Similar to index funds but trade like stocks. You can buy broad-market ETFs (e.g., VOO, SPY) or ETFs focused on specific sectors, countries, or asset classes.

They provide broad market exposure without the need for extensive research into individual companies.

4. Automate Your Investments

One of the most effective strategies for long-term investing is automation. Set up automatic monthly transfers from your checking account to your investment account. This removes the emotional component of investing and ensures you consistently contribute, regardless of market conditions. It’s also a form of dollar-cost averaging.

5. Implement Dollar-Cost Averaging

Dollar-cost averaging (DCA) is the strategy of investing a fixed amount of money at regular intervals, regardless of the market price. When prices are high, your fixed amount buys fewer shares; when prices are low, it buys more shares. Over time, this averages out your purchase price and reduces the risk of making a large investment just before a market downturn. It’s a disciplined approach that benefits long-term investors.

6. Don’t Try to Time the Market

Countless studies have shown that consistently trying to buy low and sell high is nearly impossible, even for professional investors. Focus on “time in the market” rather than “timing the market.” Long-term growth is achieved by staying invested through market ups and downs, allowing compounding to work its magic. Panic selling during downturns almost always results in missed recovery and significant losses.

7. Rebalance Your Portfolio Periodically

Over time, your portfolio’s asset allocation (the percentage you’ve allocated to stocks, bonds, etc.) will drift as some investments perform better than others. Rebalancing means adjusting your portfolio back to your original target allocation. For example, if stocks have done exceptionally well, you might sell some stock funds and buy more bond funds to maintain your desired risk level. This ensures your portfolio remains aligned with your risk tolerance and goals.

Advanced Strategies and Continued Learning

As you gain experience and confidence, you might explore more sophisticated investment strategies. However, always prioritize understanding before acting.

Active vs. Passive Investing

- Passive Investing: This is the strategy favored by many beginners and long-term investors. It involves buying and holding a diversified portfolio of low-cost index funds or ETFs, aiming to match market returns over time. It requires minimal active management.

- Active Investing: This involves making frequent trades, trying to pick individual stocks, or using actively managed mutual funds with the goal of outperforming the market. It requires significant research, time, and carries higher risk and often higher fees. While it can lead to higher returns, it often leads to underperformance compared to passive strategies after fees.

For most people learning how to start investing, passive investing is the more prudent and effective approach.

Tax-Loss Harvesting

This is an advanced strategy where you sell investments at a loss to offset capital gains and potentially reduce your taxable income. You can then repurchase a similar (but not identical) investment after 30 days to maintain your market exposure. This is typically done in taxable brokerage accounts.

Understanding Options and Futures

These are complex derivative instruments used by experienced traders for speculation or hedging. They involve significant risk and are generally not suitable for beginners. Only consider these once you have a deep understanding of market mechanics and substantial capital you are willing to lose.

Real Estate Crowdfunding and Alternative Investments

Beyond traditional stocks and bonds, you can explore platforms that pool money for real estate projects, or look into peer-to-peer lending, or even fractional ownership of alternative assets like fine art or collectibles. These can offer diversification but often come with higher risk, lower liquidity, and require more due diligence.

Continuous Education is Key

The financial world is constantly evolving. Make a habit of reading financial news from reputable sources like diaalnews, books on investing, and attending webinars. The more you learn, the better equipped you’ll be to make informed decisions and adapt your strategy as your life circumstances and market conditions change.

Explore more resources for financial literacy and investment education to deepen your knowledge.

Monitoring Your Investments and Making Adjustments

Investing isn’t a “set it and forget it” endeavor, though passive strategies require less frequent intervention. Regularly monitoring and occasionally adjusting your portfolio is crucial to staying on track with your financial goals.

Regular Portfolio Reviews

You don’t need to check your portfolio daily, which can lead to emotional decisions based on short-term fluctuations. Instead, schedule periodic reviews, perhaps quarterly or semi-annually. During these reviews:

- Check Performance: How are your investments performing relative to benchmarks and your expectations?

- Reassess Goals: Have your financial goals changed? Has your timeline shifted?

- Evaluate Risk Tolerance: Has your comfort with risk evolved? Has your financial situation become more (or less) stable?

- Rebalance: As mentioned earlier, bring your asset allocation back to your target percentages.

Staying Informed, Not Overwhelmed

Keep up with general economic news and market trends without getting caught up in daily sensationalism. Understand broad economic indicators, interest rate changes, and geopolitical events that could impact your investments over the long term. Avoid making rash decisions based on headlines or social media hype.

Adapting to Life Changes

Your investment strategy should be flexible enough to adapt to major life events:

- Job Change: Consider rolling over old 401(k)s, or adjusting contributions if your income changes.

- Marriage or Children: These events often introduce new financial goals (e.g., 529 plans) and may shift your risk tolerance.

- Major Purchases: Saving for a home or another significant expense might require temporarily adjusting your investment contributions or reallocating funds.

- Approaching Retirement: As you near retirement, it’s common to shift your portfolio from growth-oriented (more stocks) to capital-preservation-oriented (more bonds) to protect your accumulated wealth.

Common Investing Mistakes to Avoid for Beginners

Learning how to start investing means not just knowing what to do, but also what pitfalls to steer clear of. Avoiding these common mistakes can save you significant time and money.

1. Delaying Getting Started

This is perhaps the biggest mistake of all. The longer you wait, the less time compound interest has to work its magic. Even small amounts invested early on can far surpass larger amounts invested later. “The best time to plant a tree was 20 years ago. The second best time is now.” The same applies to investing.

2. Investing Without an Emergency Fund

As discussed, an emergency fund prevents you from needing to sell investments prematurely, especially during market downturns when you’d lock in losses. Without this safety net, unexpected expenses can force poor investment decisions.

3. Following the Crowd or Hype

Don’t invest in something just because everyone else is, or because a particular stock is “trending” online. Hype-driven investments often lead to bubbles and subsequent crashes. Do your own research, understand the underlying asset, and stick to your well-researched strategy.

4. Emotional Investing (Panic Selling or FOMO)

Emotions are the enemy of successful investing. Panic selling during a market correction means you’re locking in losses and missing out on the inevitable recovery. Conversely, buying out of “Fear Of Missing Out” (FOMO) when prices are skyrocketing often leads to buying at the peak. Stick to your long-term plan and automate your contributions to remove emotion from the equation.

5. Not Diversifying Enough

Putting all your money into one stock, one sector, or one type of asset is incredibly risky. A diversified portfolio spreads risk, protecting you from significant losses if a single investment tanks.

6. Ignoring Fees and Expenses

Even small fees, like high expense ratios on mutual funds or frequent trading commissions, can significantly erode your returns over decades. Always be mindful of the costs associated with your investments and choose low-cost options where possible.

7. Lack of Continuous Learning

The investment landscape is dynamic. Not staying informed about basic economic principles, new investment vehicles, or changes in tax laws can lead to missed opportunities or outdated strategies. Make education a continuous part of your investment journey.

Learn more about common investing pitfalls and how to avoid them to safeguard your portfolio.

Conclusion: Your First Step Towards a Prosperous Future

Learning how to start investing is not just about numbers and charts; it’s about taking control of your financial destiny and building a more secure future. While the journey may seem daunting at first, breaking it down into manageable steps reveals a clear path forward. By understanding the basics, preparing your finances, setting clear goals, managing risk, and choosing the right vehicles and platforms, you are well on your way to becoming a confident and successful investor.

Remember, consistency is key. Small, regular contributions made over a long period, coupled with the incredible power of compound interest, can lead to substantial wealth accumulation. Don’t be discouraged by market fluctuations; stay disciplined, avoid emotional decisions, and continuously educate yourself.

The year 2026 offers more opportunities and resources than ever before for individuals to participate in the financial markets. Take that first step today. Start small, stay consistent, and watch your financial future grow. Your future self will thank you for making the decision to start investing now.

Frequently Asked Questions

Q1: What’s the absolute minimum I need to start investing?

A1: You can start investing with surprisingly little! Many online brokerage platforms and robo-advisors allow you to open an account with no minimum balance. Some even offer fractional shares, meaning you can buy a portion of a high-priced stock or ETF for as little as $5 or $10. The key is to establish a consistent habit of contributing regularly, even if it’s a small amount like $25 or $50 per month.

Q2: Is it too late to start investing in 2026?

A2: It is never too late to start investing. While starting early offers the greatest advantage due to compounding, any time you begin is better than never. The principles of investing – diversification, long-term focus, and dollar-cost averaging – remain effective regardless of your age or current year. Focus on your personal goals and time horizon, and remember that even a few years of consistent investing can make a significant difference.

Q3: Should I invest in individual stocks or ETFs/mutual funds as a beginner?

A3: For most beginners, it is highly recommended to start with diversified options like Exchange-Traded Funds (ETFs) or mutual funds, particularly index funds. These vehicles offer instant diversification across many companies, sectors, or even entire markets, significantly reducing the risk associated with investing in single stocks. Individual stock picking requires substantial research, carries higher risk, and is generally better suited for more experienced investors.

Q4: How do I choose the right brokerage account for a beginner?

A4: When choosing a brokerage, consider factors such as fees (look for commission-free trades for stocks and ETFs), minimum investment requirements, available investment options (do they offer what you want to invest in?), educational resources, user-friendliness of the platform, and customer support. Popular beginner-friendly options often include Fidelity, Charles Schwab, Vanguard, and robo-advisors like Betterment or Wealthfront for automated investing.

Q5: How much risk should I take when I’m just starting?

A5: Your appropriate level of risk depends on your time horizon, financial stability, and personal comfort with market fluctuations. As a beginner, it’s often wise to start with a moderate level of risk, typically achieved through a diversified portfolio of mostly growth-oriented assets (like stock ETFs) balanced with some more stable assets (like bond ETFs). As you gain experience and your financial situation evolves, you can adjust your risk exposure. Never invest money you cannot afford to lose, especially in highly speculative assets.

How to Start Investing: Your Comprehensive Guide to Building Wealth in 2026

Affiliate disclosure: This article may contain affiliate links. Recommendations are independent and editorially driven.

The journey to financial independence often begins with a single, crucial step: learning how to start investing. For many, the world of investing seems complex, intimidating, and reserved for financial gurus. However, in 2026, with an abundance of accessible platforms, educational resources, and diverse investment vehicles, there has never been a better time for individuals from all walks of life to begin building their wealth.

Investing isn’t just about accumulating money; it’s about making your money work for you, harnessing the power of compound interest, and achieving long-term financial goals, whether that’s buying a home, funding your children’s education, or securing a comfortable retirement. This comprehensive guide will demystify the process, breaking down everything you need to know about how to start investing, from foundational principles to advanced strategies.

We’ll walk you through assessing your financial readiness, setting realistic goals, understanding different investment types, managing risk, and choosing the right platforms. By the end of this guide, you’ll have a clear roadmap and the confidence to take your first steps into the exciting world of investing, transforming your financial future.

Understanding the Basics: Why Investing Matters

Before diving into the mechanics of how to start investing, it’s crucial to grasp the fundamental ‘why.’ Investing isn’t a get-rich-quick scheme; it’s a long-term strategy designed to grow your capital over time, outpacing inflation and building substantial wealth. Here’s why it’s a cornerstone of sound financial planning:

The Power of Compounding: Your Money’s Best Friend

Compound interest is often called the “eighth wonder of the world.” It’s the process where the returns on your investments are reinvested, generating their own returns. Over time, this creates an exponential growth effect. Imagine you invest $1,000 and earn 7% in the first year. You now have $1,070. In the second year, you earn 7% on $1,070, not just your original $1,000. This snowball effect is why starting early is paramount. Even small, consistent investments can accumulate into significant wealth over decades.

Beating Inflation: Protecting Your Purchasing Power

Inflation is the silent assassin of savings. It’s the rate at which the general level of prices for goods and services is rising, and consequently, the purchasing power of currency is falling. If your money is just sitting in a standard savings account earning a negligible interest rate, its real value is eroding year after year. Investing, particularly in assets that historically outperform inflation like stocks or real estate, helps your money retain and even grow its purchasing power, ensuring your future self can afford more, not less.

Achieving Financial Goals: From Retirement to Education

Specific financial goals often require substantial capital. Whether it’s a down payment on a house, funding a child’s college education, or securing a comfortable retirement, saving alone often isn’t enough. Investing provides the accelerated growth needed to reach these milestones. By aligning your investment strategy with your goals, you can calculate the approximate amount you need to invest regularly and the expected rate of return to hit your targets within a desired timeframe.

Diversification and Risk Mitigation Over Time

While investing always carries some risk, a well-diversified portfolio can mitigate specific risks. Spreading your investments across various asset classes, industries, and geographies reduces the impact of a poor performance by any single investment. Furthermore, over long periods, market fluctuations tend to smooth out, making long-term investing generally less risky than short-term trading.

[INLINE IMAGE 1: place after second H2 | alt=”how to start investing concept illustration”]

Assessing Your Financial Readiness: The Pre-Investment Checklist

Before you even think about opening a brokerage account, it’s essential to ensure your personal finances are in order. Skipping these crucial preliminary steps can lead to unnecessary stress and potentially jeopardize your investments.

1. Clear Your High-Interest Debt

This is arguably the most critical step. High-interest debt, such as credit card balances or personal loans, can carry annual interest rates of 15% to 25% or even higher. It’s extremely difficult for investments to consistently generate returns high enough to outpace these costs. Paying off high-interest debt offers a guaranteed “return” equal to the interest rate you avoid paying, making it a powerful first investment in itself. Focus on a debt repayment strategy, like the snowball or avalanche method, before allocating significant funds to investments.

2. Build a Robust Emergency Fund

Life is unpredictable, and unexpected expenses can derail your financial plans. An emergency fund is a readily accessible savings account holding 3 to 6 months’ worth of essential living expenses. This fund acts as a financial safety net, preventing you from having to sell investments prematurely (potentially at a loss) or incur new debt when faced with job loss, medical emergencies, or car repairs. This fund should be liquid, meaning it’s easy to access, typically in a high-yield savings account.

3. Understand Your Monthly Budget and Cash Flow

You can’t effectively invest if you don’t know where your money is going. Creating a detailed monthly budget allows you to track income and expenses, identify areas for savings, and determine how much money you can realistically allocate to investing each month without straining your finances. Knowing your cash flow helps you make consistent contributions, which is key to long-term investment success.

- Track Income: List all sources of income.

- Track Expenses: Categorize fixed (rent, loan payments) and variable (groceries, entertainment) expenses.

- Identify Savings Opportunities: Look for areas to reduce spending and redirect those funds to your investment portfolio.

4. Define Your Investment Capital

Once high-interest debt is managed and your emergency fund is robust, determine how much money you can comfortably set aside for investing on a regular basis. This doesn’t have to be a large sum to start. Many platforms allow you to begin investing with as little as $50 or $100 per month. The key is consistency. Even small, regular contributions can grow substantially over time due to compounding.

Setting Your Investment Goals and Time Horizon

Knowing why you’re investing is just as important as knowing how to start investing. Your goals will dictate your investment strategy, risk tolerance, and the types of assets you choose.

Short-Term Goals (1-5 Years)

These goals typically include saving for a down payment on a car, a vacation, or a small home renovation. For short-term goals, capital preservation and liquidity are more important than aggressive growth.

- Investment Focus: Low-risk, highly liquid assets.

- Examples: High-yield savings accounts, Certificates of Deposit (CDs), money market accounts, short-term bond funds.

- Risk Tolerance: Very low. You cannot afford significant fluctuations.

Medium-Term Goals (5-15 Years)

These might include saving for a child’s college education, a larger home down payment, or starting a business. With a slightly longer time horizon, you can afford to take on a bit more risk for potentially higher returns.

- Investment Focus: A balanced approach between growth and stability.

- Examples: Diversified portfolios including a mix of stocks (through ETFs or mutual funds) and bonds.

- Risk Tolerance: Moderate. You have time to recover from minor market downturns.

Long-Term Goals (15+ Years)

Retirement savings is the quintessential long-term goal. With decades ahead, you can embrace more risk for maximum growth potential.

- Investment Focus: Growth-oriented assets.

- Examples: Predominantly equities (stocks, stock ETFs, growth mutual funds), potentially some real estate or alternative investments as you become more experienced.

- Risk Tolerance: High to moderate. Market volatility over short periods is less concerning as you have ample time for recovery.

Matching Goals to Your Investment Horizon

It’s crucial to align your investment horizon with the types of investments you choose. Attempting to achieve short-term goals with volatile, long-term assets can lead to losses if you need to liquidate during a market downturn. Conversely, using conservative, short-term instruments for long-term goals might leave you short of your target due to insufficient growth. This step is fundamental to a successful strategy when learning how to start investing.

Understanding Risk and Your Risk Tolerance

Risk is an inherent part of investing. There’s no such thing as a risk-free investment that offers significant returns. However, understanding different types of risk and your personal tolerance for it is paramount before you begin investing.

What is Investment Risk?

Investment risk refers to the probability or likelihood of an actual return being different from the expected return. This includes the possibility of losing some or all of your initial investment. Common types of risk include:

- Market Risk: The risk that the entire market or a specific sector will decline, impacting your investments regardless of their individual performance.

- Inflation Risk: The risk that inflation will erode the purchasing power of your investment returns.

- Interest Rate Risk: The risk that changes in interest rates will negatively affect the value of fixed-income investments like bonds.

- Liquidity Risk: The risk that you may not be able to sell an investment quickly enough at a fair market price (e.g., real estate vs. publicly traded stocks).

- Credit Risk: The risk that a bond issuer will default on its payments (relevant for bondholders).

Assessing Your Personal Risk Tolerance

Your risk tolerance is your willingness and ability to take on financial risk. It’s influenced by several factors:

- Time Horizon: As discussed, longer horizons generally allow for higher risk.

- Financial Stability: A robust emergency fund and stable income allow for greater risk.

- Personality and Emotions: How will you react to market downturns? Can you stomach watching your portfolio temporarily lose value without panic-selling?

- Investment Knowledge: Greater understanding often leads to more comfortable risk-taking.

Many online brokerage platforms and financial advisors offer risk assessment questionnaires designed to help you quantify your tolerance. Be honest with yourself. It’s better to start conservatively and gradually increase your risk exposure as you gain experience and comfort, rather than taking on too much risk and making impulsive decisions during market volatility.

Understanding market volatility and how to manage it is a key aspect of building a resilient investment strategy.

Exploring Investment Vehicles: Where to Put Your Money

Once you’ve prepared your finances and set your goals, the next step in how to start investing is to understand the various investment vehicles available. Each comes with its own risk-reward profile and is suitable for different goals.

1. Stocks (Equities)

When you buy a stock, you’re purchasing a small piece of ownership in a public company. As the company grows and profits, the value of its stock can increase, and you might receive dividends (a portion of the company’s earnings).

- Pros: High growth potential over the long term; ownership in successful companies.

- Cons: High volatility; individual stocks can be risky; requires research.

- Best For: Long-term growth, higher risk tolerance.

2. Bonds (Fixed Income)

Bonds are essentially loans you make to governments or corporations. In return, the issuer promises to pay you regular interest payments and return your principal investment at a specified maturity date.

- Pros: Generally less volatile than stocks; provides regular income; good for capital preservation.

- Cons: Lower growth potential than stocks; susceptible to interest rate risk.

- Best For: Capital preservation, income generation, lower risk tolerance, diversifying a portfolio.

3. Mutual Funds

A mutual fund is a professionally managed portfolio that pools money from many investors to purchase a diverse collection of stocks, bonds, or other securities.

- Pros: Instant diversification; professional management; convenient.

- Cons: Management fees (expense ratios) can eat into returns; lack of control over individual holdings.

- Best For: Beginners seeking diversification and professional management without picking individual securities.

4. Exchange-Traded Funds (ETFs)

ETFs are similar to mutual funds in that they hold a basket of securities, but they trade on stock exchanges throughout the day like individual stocks. They often track an index (e.g., S&P 500), a sector, or a commodity.

- Pros: Diversification; typically lower expense ratios than actively managed mutual funds; flexibility to trade throughout the day.

- Cons: Trading fees (though many brokers offer commission-free ETF trading); market price can differ slightly from net asset value.

- Best For: Cost-effective diversification, broad market exposure, suitable for all risk tolerances depending on the ETF’s holdings.

5. Real Estate

Investing in real estate can involve buying physical properties (residential, commercial), Real Estate Investment Trusts (REITs), or real estate crowdfunding.

- Pros: Potential for capital appreciation and rental income; tangible asset.

- Cons: Illiquid; high upfront costs (for physical property); management responsibilities.

- Best For: Long-term investors, those with significant capital or seeking diversification beyond traditional securities. REITs offer a more liquid way to invest in real estate.

6. Certificates of Deposit (CDs)

CDs are savings certificates with a fixed maturity date and a fixed interest rate. You deposit a sum of money for a set period, and the bank pays you interest.

- Pros: Very low risk; predictable returns; FDIC-insured up to certain limits.

- Cons: Lower returns; funds are locked in for the term (though penalties for early withdrawal exist).

- Best For: Short-term savings goals, emergency fund overflow, very low risk tolerance.

7. Cryptocurrencies (e.g., Bitcoin, Ethereum)

Digital or virtual currencies that use cryptography for security and operate independently of a central bank.

- Pros: Potentially very high returns; innovative technology.

- Cons: Extremely volatile; largely unregulated; complex to understand; susceptible to scams and hacks.

- Best For: Investors with a very high risk tolerance, comfortable with significant fluctuations, and only with a small portion of their overall portfolio.

[INLINE IMAGE 2: place after fourth H2 | alt=”how to start investing comparison illustration”]

Here’s a comparison table summarizing some key characteristics of popular investment vehicles:

| Investment Type | Primary Benefit | Typical Risk Level | Liquidity | Minimum Investment (approx.) |

|---|---|---|---|---|

| Individual Stocks | High Growth Potential | High | High | Cost of one share (e.g., $50-$500+) |

| Bonds | Income, Stability | Low to Moderate | Moderate to High | $1,000+ (individual), lower for bond funds |

| Mutual Funds | Diversification, Professional Management | Moderate | Moderate (daily trading) | $500-$3,000+ (initial) |

| Exchange-Traded Funds (ETFs) | Diversification, Low Cost, Flexibility | Low to High (depends on holdings) | High (intra-day trading) | Cost of one share (e.g., $20-$300+) |

| Real Estate (REITs) | Income, Growth, Inflation Hedge | Moderate | High (REITs) | Cost of one REIT share (e.g., $50-$200+) |

| Certificates of Deposit (CDs) | Guaranteed Returns, Capital Preservation | Very Low | Low (funds locked) | $500-$1,000+ |

Choosing the Right Investment Accounts and Platforms

Once you know what you want to invest in, you need a place to do it. The type of account and platform you choose can significantly impact your investment journey. When considering how to start investing, this step is more practical than theoretical.

Types of Investment Accounts

The account you choose will determine tax implications, contribution limits, and how you access your money.

- Taxable Brokerage Accounts:

- Description: Standard investment accounts where you pay taxes on capital gains, dividends, and interest each year. No contribution limits, great flexibility.

- Best For: Short-term goals, accessible funds, investing beyond retirement limits.

- Tax-Advantaged Retirement Accounts: These are crucial for long-term wealth building due to their tax benefits.

- 401(k) or 403(b): Employer-sponsored plans. Contributions are often pre-tax (reducing current taxable income), and growth is tax-deferred until retirement. Many employers offer matching contributions, which is essentially free money.

- Individual Retirement Accounts (IRAs):

- Traditional IRA: Contributions may be tax-deductible, and growth is tax-deferred. Withdrawals in retirement are taxed as ordinary income.

- Roth IRA: Contributions are made with after-tax money, but qualified withdrawals in retirement are completely tax-free. Excellent for those who expect to be in a higher tax bracket in retirement.

- Health Savings Account (HSA): If you have a high-deductible health plan, an HSA offers a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. It can also function as a supplemental retirement account after age 65.

- 529 Plans:

- Description: Tax-advantaged savings plans designed to encourage saving for future education costs. Earnings grow tax-free, and withdrawals for qualified educational expenses are also tax-free.

- Best For: Saving for college or vocational training.

Choosing an Investment Platform or Brokerage

With numerous online brokers available, consider these factors:

- Fees and Commissions: Look for commission-free stock and ETF trades. Be aware of expense ratios for mutual funds, account maintenance fees, or inactivity fees.

- Minimum Investment: Some platforms allow you to start with very little, offering fractional shares, while others have higher minimums for certain funds or accounts.

- Investment Options: Does the platform offer the types of investments you’re interested in (stocks, ETFs, mutual funds, bonds, crypto)?

- Tools and Resources: Look for robust research tools, educational content, portfolio analysis, and goal-setting features.

- User Experience: Is the platform intuitive and easy to navigate for beginners? Do they have a mobile app?

- Customer Support: Are they responsive and helpful?

Popular online brokerage options for beginners in 2026 often include:

- Fidelity: Known for low-cost index funds, robust research, and excellent customer service.

- Charles Schwab: Offers a wide range of investment products, low fees, and strong customer support.

- Vanguard: Famous for its low-cost index funds and ETFs, ideal for long-term passive investors.

- E*TRADE: A well-established platform with a good balance of features for beginners and experienced traders.

- Robinhood: Popular for its user-friendly interface and commission-free trading, though sometimes criticized for encouraging speculative trading.

- M1 Finance: Combines automated investing with customization, allowing you to build “pies” of investments.

- Robo-Advisors (e.g., Betterment, Wealthfront): Offer automated portfolio management based on your goals and risk tolerance, with very low minimums and management fees. They’re an excellent option for hands-off investing.

Finding the best brokerage account for beginners can significantly simplify your entry into investing.

Starting Your Investment Journey: Practical Strategies for Beginners

Once you’ve done your homework and chosen your platform, it’s time to put your plan into action. Here are some practical strategies for how to start investing effectively as a beginner.

1. Start Small and Stay Consistent

You don’t need a fortune to begin investing. Many platforms allow you to start with as little as $50 or $100. The key is to make investing a regular habit. Automate your investments if possible, setting up recurring transfers from your checking account to your investment account. This consistency, combined with compounding, is far more powerful than trying to time the market with large, infrequent contributions.

2. Embrace Diversification

The old adage “don’t put all your eggs in one basket” is particularly true for investing. Diversification means spreading your investments across different asset classes (stocks, bonds, real estate), industries, and geographical regions. This strategy reduces risk because if one investment performs poorly, others may perform well, cushioning the impact on your overall portfolio.

- Example: Instead of buying stock in just one tech company, invest in an S&P 500 index ETF, which gives you exposure to 500 of the largest U.S. companies across various sectors.

3. Consider Index Funds and ETFs (Exchange-Traded Funds)

For most beginners, individual stock picking is too risky and time-consuming. Index funds and ETFs are excellent alternatives because they offer instant diversification at a low cost.

- Index Funds: These funds passively track a specific market index (e.g., S&P 500, NASDAQ, total stock market). They aim to match the performance of the index, not beat it, and typically have very low expense ratios.

- ETFs: Similar to index funds but trade like stocks. You can buy broad-market ETFs (e.g., VOO, SPY) or ETFs focused on specific sectors, countries, or asset classes.

They provide broad market exposure without the need for extensive research into individual companies.

4. Automate Your Investments

One of the most effective strategies for long-term investing is automation. Set up automatic monthly transfers from your checking account to your investment account. This removes the emotional component of investing and ensures you consistently contribute, regardless of market conditions. It’s also a form of dollar-cost averaging.

5. Implement Dollar-Cost Averaging

Dollar-cost averaging (DCA) is the strategy of investing a fixed amount of money at regular intervals, regardless of the market price. When prices are high, your fixed amount buys fewer shares; when prices are low, it buys more shares. Over time, this averages out your purchase price and reduces the risk of making a large investment just before a market downturn. It’s a disciplined approach that benefits long-term investors.

6. Don’t Try to Time the Market

Countless studies have shown that consistently trying to buy low and sell high is nearly impossible, even for professional investors. Focus on “time in the market” rather than “timing the market.” Long-term growth is achieved by staying invested through market ups and downs, allowing compounding to work its magic. Panic selling during downturns almost always results in missed recovery and significant losses.

7. Rebalance Your Portfolio Periodically

Over time, your portfolio’s asset allocation (the percentage you’ve allocated to stocks, bonds, etc.) will drift as some investments perform better than others. Rebalancing means adjusting your portfolio back to your original target allocation. For example, if stocks have done exceptionally well, you might sell some stock funds and buy more bond funds to maintain your desired risk level. This ensures your portfolio remains aligned with your risk tolerance and goals.

Advanced Strategies and Continued Learning

As you gain experience and confidence, you might explore more sophisticated investment strategies. However, always prioritize understanding before acting.

Active vs. Passive Investing

- Passive Investing: This is the strategy favored by many beginners and long-term investors. It involves buying and holding a diversified portfolio of low-cost index funds or ETFs, aiming to match market returns over time. It requires minimal active management.

- Active Investing: This involves making frequent trades, trying to pick individual stocks, or using actively managed mutual funds with the goal of outperforming the market. It requires significant research, time, and carries higher risk and often higher fees. While it can lead to higher returns, it often leads to underperformance compared to passive strategies after fees.

For most people learning how to start investing, passive investing is the more prudent and effective approach.

Tax-Loss Harvesting

This is an advanced strategy where you sell investments at a loss to offset capital gains and potentially reduce your taxable income. You can then repurchase a similar (but not identical) investment after 30 days to maintain your market exposure. This is typically done in taxable brokerage accounts.

Understanding Options and Futures

These are complex derivative instruments used by experienced traders for speculation or hedging. They involve significant risk and are generally not suitable for beginners. Only consider these once you have a deep understanding of market mechanics and substantial capital you are willing to lose.

Real Estate Crowdfunding and Alternative Investments

Beyond traditional stocks and bonds, you can explore platforms that pool money for real estate projects, or look into peer-to-peer lending, or even fractional ownership of alternative assets like fine art or collectibles. These can offer diversification but often come with higher risk, lower liquidity, and require more due diligence.

Continuous Education is Key

The financial world is constantly evolving. Make a habit of reading financial news from reputable sources like diaalnews, books on investing, and attending webinars. The more you learn, the better equipped you’ll be to make informed decisions and adapt your strategy as your life circumstances and market conditions change.

Explore more resources for financial literacy and investment education to deepen your knowledge.

Monitoring Your Investments and Making Adjustments

Investing isn’t a “set it and forget it” endeavor, though passive strategies require less frequent intervention. Regularly monitoring and occasionally adjusting your portfolio is crucial to staying on track with your financial goals.

Regular Portfolio Reviews

You don’t need to check your portfolio daily, which can lead to emotional decisions based on short-term fluctuations. Instead, schedule periodic reviews, perhaps quarterly or semi-annually. During these reviews:

- Check Performance: How are your investments performing relative to benchmarks and your expectations?

- Reassess Goals: Have your financial goals changed? Has your timeline shifted?

- Evaluate Risk Tolerance: Has your comfort with risk evolved? Has your financial situation become more (or less) stable?

- Rebalance: As mentioned earlier, bring your asset allocation back to your target percentages.

Staying Informed, Not Overwhelmed

Keep up with general economic news and market trends without getting caught up in daily sensationalism. Understand broad economic indicators, interest rate changes, and geopolitical events that could impact your investments over the long term. Avoid making rash decisions based on headlines or social media hype.

Adapting to Life Changes

Your investment strategy should be flexible enough to adapt to major life events:

- Job Change: Consider rolling over old 401(k)s, or adjusting contributions if your income changes.

- Marriage or Children: These events often introduce new financial goals (e.g., 529 plans) and may shift your risk tolerance.

- Major Purchases: Saving for a home or another significant expense might require temporarily adjusting your investment contributions or reallocating funds.

- Approaching Retirement: As you near retirement, it’s common to shift your portfolio from growth-oriented (more stocks) to capital-preservation-oriented (more bonds) to protect your accumulated wealth.

Common Investing Mistakes to Avoid for Beginners

Learning how to start investing means not just knowing what to do, but also what pitfalls to steer clear of. Avoiding these common mistakes can save you significant time and money.

1. Delaying Getting Started

This is perhaps the biggest mistake of all. The longer you wait, the less time compound interest has to work its magic. Even small amounts invested early on can far surpass larger amounts invested later. “The best time to plant a tree was 20 years ago. The second best time is now.” The same applies to investing.

2. Investing Without an Emergency Fund

As discussed, an emergency fund prevents you from needing to sell investments prematurely, especially during market downturns when you’d lock in losses. Without this safety net, unexpected expenses can force poor investment decisions.

3. Following the Crowd or Hype

Don’t invest in something just because everyone else is, or because a particular stock is “trending” online. Hype-driven investments often lead to bubbles and subsequent crashes. Do your own research, understand the underlying asset, and stick to your well-researched strategy.

4. Emotional Investing (Panic Selling or FOMO)

Emotions are the enemy of successful investing. Panic selling during a market correction means you’re locking in losses and missing out on the inevitable recovery. Conversely, buying out of “Fear Of Missing Out” (FOMO) when prices are skyrocketing often leads to buying at the peak. Stick to your long-term plan and automate your contributions to remove emotion from the equation.

5. Not Diversifying Enough

Putting all your money into one stock, one sector, or one type of asset is incredibly risky. A diversified portfolio spreads risk, protecting you from significant losses if a single investment tanks.

6. Ignoring Fees and Expenses

Even small fees, like high expense ratios on mutual funds or frequent trading commissions, can significantly erode your returns over decades. Always be mindful of the costs associated with your investments and choose low-cost options where possible.

7. Lack of Continuous Learning

The investment landscape is dynamic. Not staying informed about basic economic principles, new investment vehicles, or changes in tax laws can lead to missed opportunities or outdated strategies. Make education a continuous part of your investment journey.

Learn more about common investing pitfalls and how to avoid them to safeguard your portfolio.

Conclusion: Your First Step Towards a Prosperous Future

Learning how to start investing is not just about numbers and charts; it’s about taking control of your financial destiny and building a more secure future. While the journey may seem daunting at first, breaking it down into manageable steps reveals a clear path forward. By understanding the basics, preparing your finances, setting clear goals, managing risk, and choosing the right vehicles and platforms, you are well on your way to becoming a confident and successful investor.

Remember, consistency is key. Small, regular contributions made over a long period, coupled with the incredible power of compound interest, can lead to substantial wealth accumulation. Don’t be discouraged by market fluctuations; stay disciplined, avoid emotional decisions, and continuously educate yourself.

The year 2026 offers more opportunities and resources than ever before for individuals to participate in the financial markets. Take that first step today. Start small, stay consistent, and watch your financial future grow. Your future self will thank you for making the decision to start investing now.

Frequently Asked Questions

Q1: What’s the absolute minimum I need to start investing?

A1: You can start investing with surprisingly little! Many online brokerage platforms and robo-advisors allow you to open an account with no minimum balance. Some even offer fractional shares, meaning you can buy a portion of a high-priced stock or ETF for as little as $5 or $10. The key is to establish a consistent habit of contributing regularly, even if it’s a small amount like $25 or $50 per month.

Q2: Is it too late to start investing in 2026?

A2: It is never too late to start investing. While starting early offers the greatest advantage due to compounding, any time you begin is better than never. The principles of investing – diversification, long-term focus, and dollar-cost averaging – remain effective regardless of your age or current year. Focus on your personal goals and time horizon, and remember that even a few years of consistent investing can make a significant difference.

Q3: Should I invest in individual stocks or ETFs/mutual funds as a beginner?

A3: For most beginners, it is highly recommended to start with diversified options like Exchange-Traded Funds (ETFs) or mutual funds, particularly index funds. These vehicles offer instant diversification across many companies, sectors, or even entire markets, significantly reducing the risk associated with investing in single stocks. Individual stock picking requires substantial research, carries higher risk, and is generally better suited for more experienced investors.

Q4: How do I choose the right brokerage account for a beginner?

A4: When choosing a brokerage, consider factors such as fees (look for commission-free trades for stocks and ETFs), minimum investment requirements, available investment options (do they offer what you want to invest in?), educational resources, user-friendliness of the platform, and customer support. Popular beginner-friendly options often include Fidelity, Charles Schwab, Vanguard, and robo-advisors like Betterment or Wealthfront for automated investing.

Q5: How much risk should I take when I’m just starting?

A5: Your appropriate level of risk depends on your time horizon, financial stability, and personal comfort with market fluctuations. As a beginner, it’s often wise to start with a moderate level of risk, typically achieved through a diversified portfolio of mostly growth-oriented assets (like stock ETFs) balanced with some more stable assets (like bond ETFs). As you gain experience and your financial situation evolves, you can adjust your risk exposure. Never invest money you cannot afford to lose, especially in highly speculative assets.